Three Financial Planning Strategies During a Down Market

I remember the first time I had the wind knocked out of me. The day was unseasonably warm, and I was 8, lying in my dad’s arms in a hammock. I started to doze off and rolled out of the hammock, falling back-first onto the Mexican tile. I remember gasping for air, but I had the unusual feeling of none entering my body. I looked to my dad, fearful as to what was happening. And he arose quickly to comfort me until my breathing began again. Sure enough, after a long 10-15 seconds, the air started to flow, and things were back to normal. I was shaken, but the day progressed and we went on to feed the neighbor’s horses and fish for bass.

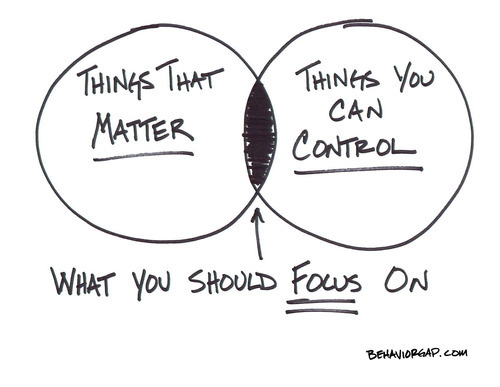

I say this because that’s how most investors feel right now. Three months ago we were writing about all-time market highs and now everyday life feels surreal. We’ve all had the wind knocked out of us. It’s at times like this that my favorite Carl Richards Venn diagram sketch comes to mind and reminds me where to place my attention.

Below we will consider a few planning strategies that are both worth focusing on and within our control.

1. Converting traditional IRA dollars to a Roth IRA

2. Moving money from an IRA to an HSA

3. Paying restricted stock options taxes early via filing form 83(b)

Convert traditional IRA dollars to a Roth IRA

Converting IRA’s to Roth IRA’s is a common strategy of paying income taxes at a known and hopefully lower tax rate now than in the future. (Justin goes into more detail about when and why you would want to complete a Roth conversion in his blog post HERE.) The main “benefit” of doing a Roth conversion in a discounted market is that we can pay taxes on a lower conversion amount, and any future appreciation in our Roth is tax-free.

Let’s say we are in the 22% tax bracket, and we own a small-cap holding that is down 35% due to COVID-19 travel, trade, and work restrictions. Our presumed new tax rate on converting those shares from an IRA to a Roth IRA would be (22% * (1-.35)) = 14.3% effective tax bracket. This strategy could be even more advantageous for the person whose 2020 income will be dramatically lower than normal.

Make a QHFD (Qualified Health Savings Account Funding Distribution)

A QHFD is a one-time tax-free transfer from an IRA into an HSA. The hope is to then withdraw those funds tax-free and avoid taxes entirely. The maximum you can transfer is $7,100 if you have family coverage and $3,550 if you have self-only coverage. QHFDs have always been useful when you have medical expenses coming up and you want to pay for them with tax-free dollars. But today, (similar to the Roth conversion mentioned above) a QHFD could be a way to transfer the funds from your IRA at their currently depreciated values, tax-free, and invest them within your HSA. Any appreciation within your HSA is tax-free if used for qualifying healthcare expenses in your lifetime. (Note: a QHFD will also count towards your RMD for the year, but remember that no RMD’s are due in 2020 due to the CARES Act.)

NOTE: A QHFD transfer added to any other contributions cannot exceed your annual HSA contribution limit ($7,100 for families and $3,550 for singles). In other words, you can’t “double-up” your annual contributions with the QHFD.

Pay Restricted Stock Options Taxes Early Via Filing Form 83(b)

This strategy typically works best for individuals who are issued restricted stock, and the current valuation is low compared to the expected value when the shares vest. When you submit your 83(b) election, you choose to pay taxes on your restricted shares at today’s valuation. Any gains between now and when the shares vest will be taxed at capital gains rates instead of income tax rates. Keep in mind that you must notify the IRS and your employer of your 83(b) election within 30 days of being issued the restricted shares. This strategy will backfire if the shares drop below their current valuation before vesting, or if you leave the company before vesting. If you want to learn more about best-case vs. worst-case scenarios and how to complete this filing then you can read more about it HERE.

Closing

These three aren’t the only strategies available, but they could be a way to benefit from what can seem like getting the wind knocked out of you. Be aware that every person’s financial and tax situation is different and the above might not make sense for you. We’re already working through these strategies for our clients, but feel free to give us a call or shoot us an email if you’d like to talk through any of the above.

Stephen Boatman

Latest posts by Stephen Boatman (see all)

- How to Calculate and Maximize Your Social Security Benefit - May 19, 2023

- An Unaffordable Housing Market: Why and What’s Next? - March 14, 2023

- $500 Billion Student Loan Forgiveness Update ($10k/$20k, New IDR Plan, 0% Interest Ending) - October 20, 2022