An Unaffordable Housing Market: Why and What’s Next?

The cost of home ownership has risen to an all-time high over the past 24 months, and there are three main reasons for this:

- Increasing interest rates

- Euphoric buying

- Constricted supply

Are current home prices and interest rates sustainable? I think we’d all agree the answer is “no,” but what story is the data telling us? And what can we expect to happen going forward?

Below we’ll discuss home affordability, mortgage rates, and how demand in the market is responding.

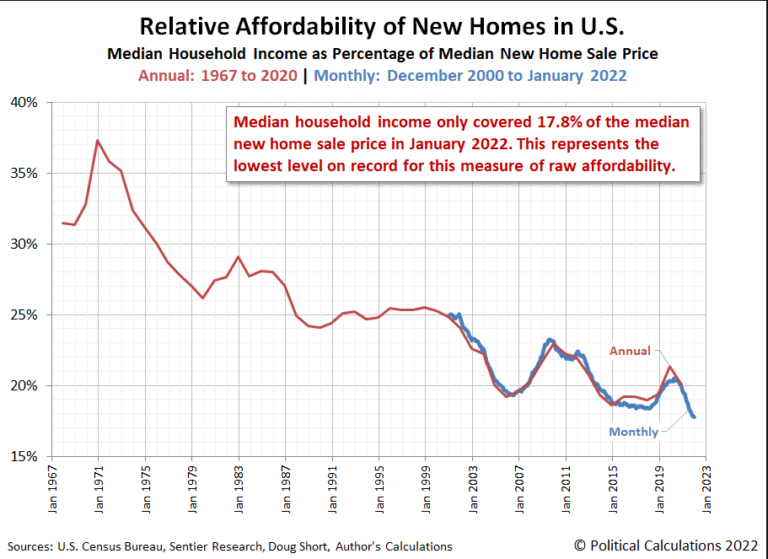

Home Affordability

In early 2022 homes sold for up to 7.8 times the median income. That is the highest price-to-median income ratio in the past 40+ years. At this price point, most buyers are institutions and wealthy individuals; most home prices are out of reach for the median income earner.

Interest Rates and Mortgage Rates

Unless you live in a cave, you are likely aware of the Fed raising the interest rate they charge banks. This rate hike increases mortgage interest rates that the banks charge homebuyers. The chart below shows how fast the Fed has raised rates, which makes owning a home, typically 80%-90% debt, much more expensive. Below is the fed funds rate from Jan 2006 to early March 2023. As of March 6, 2023, the target rate was 4.5% – 4.75%.

Euphoric Buying

Below you can see that mortgage interest rates hit a floor in 2020/2021 between 2% and 3%. This caused a flood to the housing market for first, second, and third homes due to lower financing costs. Home prices increased, and current homeowners could refinance and lower their monthly living expenses or sell and cash out. And while new home buyers had to deal with higher home prices, many could keep their monthly costs stagnant due to the lower rates. This is a recipe for a historically sticky home buyer. Because their current holding costs are so low compared to the current market, moving simply isn’t an option for most.

Constricted Supply

As WisdomTree’s Jeff Weniger points out in the chart below, buying more house has gotten extremely expensive. Moving from one $500,000 house ($300,000 mortgage) to another could cost someone more than $600/mo! To buy just $100,000 more house (maybe a bit more square footage, another bathroom, or perhaps a better neighborhood) could double your payment. Because of the lack of wage growth to keep up with these prices, combined with everyone staying put in their home, supply is low.

In the chart below, you can see that the median mortgage payment for homebuyers (of both existing and new homes) jumped from $1,500 in 2020 to $2,500 in 2023.

Rent vs. Buy

This rent vs. buy calculator from a 2018 NY Times article (NY Times login is required to access calculator) shows that purchasing a home for $450k at 2.75% in 2021 was comparable to renting a place for $1,725/mo. But now, with rising interest rates, a $450k home purchase at 6.8% is comparable to $2,534/mo rent! A difference of $809 for the same-priced home. If you want a free link to a rent vs. buy calculator, use the option HERE.

Home or monthly rental expenses typically cost 25% – 35% of net income. This means that in order to live in a $450k home, your household NET income should be between $7,234.29/mo or $86,811/yr ($112.5k gross) and $10,136/mo or $121,632/yr ($163,500 gross). With only 18% of Americans earning over $150k/yr (gross) as a household, the pool for qualified buyers is shrinking, meaning demand is shrinking.

Housing Supply and Demand

As mortgage rates stay high, housing demand will likely continue to decrease because it’s more expensive to purchase a home than rent. This leads to decreased home flipping and speculative buying, which leaves homes on the market for longer periods. These shifts could soak up more cash as people attempt to avoid the higher interest rates by paying cash for properties, home improvements, or larger down payments.

Supply is growing, but only slightly. Most people are more inclined to improve their current home rather than move and accept a higher interest rate on their mortgage. The only noticeable increase in housing supply will either come from new builders, estates, or buyers who can no longer keep their homes due to loss of income or an increase in variable rates. If the housing supply increases dramatically, we can expect a decrease in home prices.

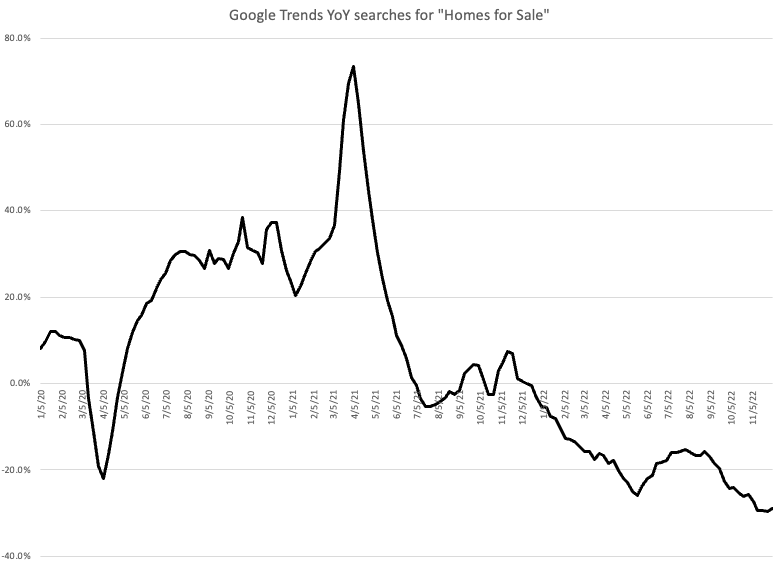

You can also see a decrease in home-buying interest based on Google searches.

Due to the decrease in home buyer interest, there has been an increase in price cuts, as seen below.

This could lead to actual home sale prices decreasing by the most significant amount since the 2008-09 housing crisis. The chart below may not look like much, but remember that most houses are bought with debt. So if you placed a 10% down payment on a home and it decreases in value by 10%, you have lost 100% of your investment (if you sell).

What’s Next?

With current interest rates, homeowners will be less likely to give up their 3% mortgage rates for the new 6-7% mortgage rates. They will likely invest more in their current home rather than move (unless they are cash buyers.) Sellers and new home builders will be pressed to lower their listing prices to incentivize movement in a stagnant housing market. These price reductions will likely need to be significant to incentivize homeowners to move from their current low-interest rate mortgages or to make it affordable for new home buyers, assuming that the Fed holds steady on the current interest rates.

Stephen Boatman

Latest posts by Stephen Boatman (see all)

- How to Calculate and Maximize Your Social Security Benefit - May 19, 2023

- An Unaffordable Housing Market: Why and What’s Next? - March 14, 2023

- $500 Billion Student Loan Forgiveness Update ($10k/$20k, New IDR Plan, 0% Interest Ending) - October 20, 2022

{kind=link}