Giving Back: Donor Advised Fund (Part 3 of 3)

This is the third in a three part series on charitable giving. At Smith Partners Wealth Management, we love Giving Back and see it as part of our every day mission. You can read more about what we have learned and what we value on our “Lessons in Giving Back” page.

Why Use a Donor Advised Fund:

Now that we know why we should give and why a stock gift can be more advantageous than gifting cash, let’s look at a tool we can use that provides more flexibility and savings; a Donor Advised Fund (DAF). A DAF is like your own personal charitable foundation. A donor can make tax deductible gifts into it and then distribute grants to organizations they are passionate about, with no time limit. Using a DAF can provide the donor with the ability to think about the tax savings now and worry about where to gift later. DAF’s also give greater anonymity to donors if so desired, the ability to invest and grow their donations, and can be used to set a giving precedent for future generations.

How Is a Donor Advised Fund Taxed:

The majority of questions we receive about DAF’s pertain to tax treatment. Because the entire deduction occurs in the year gifted, donors don’t have to keep track of any grants out of a DAF for tax purposes, after the initial gift. We will use the same example from our previous blog post to describe the benefits of a DAF. The only difference is that this time Joe knows where he wants to give $2,000 and doesn’t yet know where to give the other $8,000 out of his $10,000 gift.

Example:

- Joe establishes his DAF (The Joe Family Foundation) at the custodian of his choosing with a $10,000 irrevocable gift of appreciated Microsoft stock in May of 2017.

- Joe then receives his tax deduction of $10,000 for the year of 2017 when he files his taxes. In gifting the appreciated stock he also avoids the capital gains tax that would have been due had he sold his shares in Microsoft.

- Joe then grants out $2,000 of his DAF (anonymously if so desired) to his church. He then has time to think about where he wants to grant the remaining $8,000 over the years with no worries about maintaining grant records for tax deductions because grants aren’t deductible, only gifts are deductible.

- Jim has the option of investing the remaining $8,000 to allow his money to grow in the Donor Advised Fund until he is ready to send out another grant. All growth in the account will only benefit the recipient of future grants.

There are some limits to the amount of tax benefit you can realize based on AGI and the type of asset gifted which you can look into further HERE. We would suggest speaking with a professional before embarking on any of the strategies suggested in this article.

Which Donor Advised Fund Custodian Should I Use:

When searching for a DAF custodian there are a few things to consider. Do you want to give locally? If so, then a local custodian such as Community Foundation of Greater Greensboro may have better knowledge of the specific needs in your area. If you already know exactly what you want to give to and seek a slightly lower fee, then someone like American Endowment Foundation (AEF) may be more helpful. Once the funds are under the custodian’s authority then you can parcel out your grants to wherever you want as long as it’s to a 501(c) (non-profit organization).

Raising The Bar On Giving:

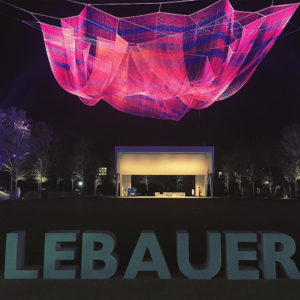

I was lucky enough to speak with the Chief Development Officer of our local DAF in Greensboro, NC (www.CFGG.org) Gordon Soenksen noted, “The best part of my job is when I can see the joy on the donor’s faces when they realize their ability to make an impact.” Soenkson pointed at an example of this impact coming to fruition through the local gift of Carolyn Weill LeBauer whose story I recommend reading and can be found by following the link above. Carolyn LeBauer set a precedent for those to come, through her generosity. She not only left a legacy in her family’s name but she brought memories and happiness to countless individuals who get to enjoy her gift every day. I believe that’s the best ROI (Return on Investment) this side of the Mississippi.

Stephen Boatman

Latest posts by Stephen Boatman (see all)

- How to Calculate and Maximize Your Social Security Benefit - May 19, 2023

- An Unaffordable Housing Market: Why and What’s Next? - March 14, 2023

- $500 Billion Student Loan Forgiveness Update ($10k/$20k, New IDR Plan, 0% Interest Ending) - October 20, 2022