Market Commentary Q1 – 2013

Margin of Safety, simply put, is the world’s oldest and cheapest form of insurance against stupidity, overconfidence and bad luck…and a few months ago, I apparently needed insurance against all three.

With the arrival of our third child on the horizon, my wife finally gave up her cool mom image and decided she needed a Minivan. After weeks of searching online, I was ecstatic (or as ecstatic as a man can get when buying a minivan) when eBay crowned me the highest bidder on a used Honda Odyssey. See, I had consulted Kelly Blue Book beforehand to assess this van’s “fair value” and discovered I was getting it for a significant discount. According to their estimate, I would be able to Trade-In this exact van to a dealer (which is typically the easiest, but least profitable way to sell a car) for around 10% more than I was paying. In other words, even though I wasn’t planning on immediately reselling the van, I could afford to be wrong by a large amount before I risked a permanent loss of capital.

What’s The Worst That Could Happen?

Despite meeting the Moscow-born used car salesman at a storage unit that held 12 other cars (with more BMWs than Minivans) in downtown Philly, everything seemed great. I inspected the van inside and out: pressed every button and turned every knob, looked through the massive stack of maintenance records, and drove it around for 10 minutes.

After registering it at the local DMV, I started my trek home and that’s when I first saw my Margin of Safety start to slip away. Once I got it up to highway speeds, I realized that the front brakes shook; something I didn’t notice on my in-town test drive. Then somewhere in the middle of Virginia I decided to listen to a book on CD and got my second “earnings disappointment”: the CD player wouldn’t load. But it wasn’t until my mechanic checked it out the next day, that I got the worst news: the timing belt had actually NOT been replaced as advertised and I’d need to spend $700 to do it now.

So there I was, needing new brakes, a timing belt, and a new CD player – grand total: 8% of my purchase price. This certainly hurt my bank account, even more so my pride, but what about my Margin of Safety? Even after these repairs, taxes, my plane ticket and gas for the trip home, my total cost was still equal to the Trade-In value. If I wanted to, I could go down to CarMax the next day, sell them the van on the spot and be no worse off. In other words, I had a Margin of Safety that insulated me from stupidity, overconfidence, and bad luck (not necessarily in that order…unless you ask my wife).

The premise of Margin of Safety is that investors should buy assets at prices far below their fair value so that the initial capital investment is never in harm’s way. I first read about it in Warren Buffett’s Berkshire Hathaway annual reports; he mentions it specifically in his 1990, 1992, and 1997 letters to shareholders. But the concept of Margin of Safety (or at least the term) originated with Buffett’s Columbia University Professor Benjamin Graham who developed the thought in the 1930’s and wrote about it in “Security Analysis” and “The Intelligent Investor”.

My Car Salesman Calls it Nyet-Nyet

Benjamin Graham, who probably also drove his wife crazy with car purchases, had a particular fondness for finding companies that met a specific and disciplined Margin of Safety requirement called the Net-Net approach: he would only buy shares of businesses selling for less than their liquidation value (net assets minus net liabilities…hence net-net). For example, take the Metal Fabrication business down the street from my office. If its only assets were the machines used in production (worth $20,000 if sold on Craigslist) and the metal in inventory (worth $15,000 sold at the scrap yard) then the net assets would be $35,000. Let’s assume the owners hold $5,000 of net debt (maybe from accounts payable and a small loan) then the “Net-Net” value would be $30,000.

Now there is surely some money to be made in repairing and fabricating metal, so if the owner offered to sell me the whole operation for $60,000 it might still be a decent investment based solely on the cash flows to the owner, but Graham wouldn’t buy it as a Net-Net. He would hold out until maybe the owner was nearing retirement, had recently experienced some slow years or was worried about rising commodity prices. If the owner would then sell the business for only $30,000, Graham would consider buying it then because of the built-in Margin of Safety. As the new owner, he could swallow a lot of bad months, maybe a workers’ compensation claim or two, even a weak commodities market, and likely still sell off the business for the sum of its parts without risking his initial capital investment.

Margin of Safety in Practice

Establishing a margin of safety requires an investor to stop asking “how right can I be?” and start asking “how wrong can I be?” It is more about stacking the odds in an investor’s favor than being 100% correct. This might seem most relevant to individual stocks, but it should apply to funds, asset allocation decisions, and all the way up to a macro economic outlook.

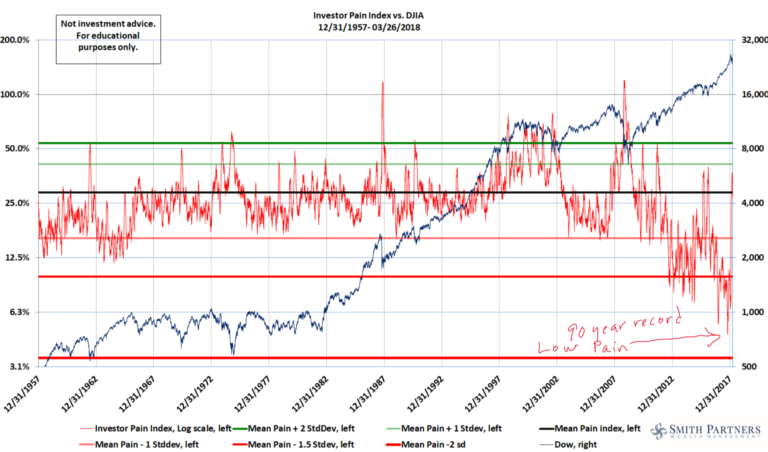

The top half of the chart shows Morningstar’s Price to Fair Value graph for every stock they analyze. When it is in the red, all stocks are selling for more than Morningstar’s estimate of their worth with no Margin of Safety (back to my van, this would be like buying for more than Kelly Blue Book value). When it is into the blue, there is some Margin of Safety. Rewind the tape to 5 years ago, April 2008, and you’ll see that Morningstar (and we) thought the market overall was pretty cheap. It had just fallen from the October 2007 highs and we thought if you bought the broad market, you’d have a roughly 15% Margin of Safety going forward. A 15% discount didn’t make us overly ecstatic but we also didn’t see a reason to sound any alarms.

Over the next year from April 2008 to April 2009 we’d see the S&P 500 drop about 40%. While some fundamentals in the market had certainly changed for the worse, you can see that in April 2009 (the market’s bottom) Morningstar thought the broad market was selling for roughly 60% of fair value (or a 40% Margin of Safety). Note that this isn’t a hindsight 20/20 estimate, this was real-time. In other words, the US Equities Minivan was surely “damaged”; but even with those repairs accounted for, you could buy it at a steep discount. That was certainly something to take advantage of and we did.

Since the 3rd Quarter of 2011, we think equities have been selling for only a moderate Margin of Safety until recently when they’ve gone up into fair value territory with nearly no Margin of Safety. This doesn’t mean broad market equities can’t or won’t go up from here. For example, you can see other fair and even overvalued times (namely the beginning of 2010 and beginning of 2011) that would have created fine opportunities to make money over the following 2 and 3 year time periods…of course you would have also had to stomach 15-20% drops in the short term that came quickly after.

The difficult aspect of investing when everything is selling for far below fair value (like 2008-2009) isn’t so much in individual selections, but more in an overall willingness to stay invested despite the inevitable bad news. Broad market (index) investing and typical asset allocations work great in this environment because a “bad” decision still gets you a great return. It is like casting a net into a school of fish: you can catch plenty of fish if you have the courage to throw it out. Conversely, in a fairly valued market (like today) the difficulty is in avoiding overpriced asset classes, sectors, and stocks in favor of those that can still provide positive returns at a time of uncertainty. It is like fishing with a single hook, for a specific type of fish, knowing if you catch the wrong kind you risk losing your line.

Margin of Safety (like any kind of insurance) is cheapest and most important when everyone else thinks you don’t need it. With another run up in equities, this quarter has been an opportunity for us to scale back some of our risks, tilt even higher toward quality, and be more concentrated in our fund and individual stock selections. We don’t think it will cost us anything in potential returns; we see it as free insurance against stupidity, overconfidence, bad luck…and even a used car salesmen.

Justin Smith

Latest posts by Justin Smith (see all)

- Tariffs and a Declaration of Parental Independence - April 11, 2025

- Quarter in Charts – Q1 2025 - April 11, 2025

- Quarter in Charts – Q4 2024 - January 22, 2025