Do Cryptoassets Like Bitcoin Belong in My Portfolio?

Back in 2004, we got a call from one of our original clients. Alice (not her real name) was a mid-60s widow who had just been on the golf course that afternoon with her younger “golfing gals.” They had been talking about the Initial Public Offering (IPO) of Google and had asked Alice if she was going to buy any.

Before Alice changed out of her spikes, she called Jonathan to ask if we thought she should own some Google shares.

Embarrassingly, we told her we didn’t see how a new internet search engine company would make any money, especially when there were already internet search engines like Yahoo, AskJeeves, and Infoseek. We had seen the dot-com bubble burst in real-time, and we might have even recounted the infamous “IPO to Bust” story, Pets.com.

Jonathan’s instinct was to tell her that adding Google might be a bad idea. And with the benefit of hindsight, he could have added that to all of the other bad Google IPO calls.

But thankfully, he returned her question with one of his own: “Would you tell me a bit more about why you want to own it?”

Her answer: “I want to be able to tell my golfing gals I own some.”

Alice and her late husband had saved well, given generously, provided for kids and grandkids, and she lived well beneath her means. Her primary sources of joy were her adult children and their spouses, grandchildren, and golf.

Alice wasn’t looking to get rich (she already was because she spent far below her target withdrawal rate), and she wasn’t looking for excess investment returns (she didn’t need them.) Alice just wanted to say, “did you see that Google today?” and see the surprised looks on the faces of her forty-something golf partners.

And so we listened to Alice and added enough Google shares to make for a meaningful investment in her mind, but not so much that if it went bust, her financial plan would feel the impact.

Stories like Alice’s can teach us a lot about how we should approach Cryptoassets. Like Google was in the beginning, concepts like Bitcoin, Ethereum, (even Dogecoin) are challenging to understand, come with an abundance of hype and opinions (both good and bad), and have the potential to either change the future or become a forgotten investment fad.

To understand the potential role of Cryptoassets in your portfolio, one first needs to answer two questions: “What do I know about Cryptoassets?” and “Why do I want to own Cryptoassets?”

What Do I Know About Cryptoassets?

As of July 15, 2021, there is a market for 10,904 unique cryptocurrencies, listed on 389 exchanges, with a Market Cap of $1,307,098,058,717. Bitcoin has dominance, with 45.6% of the market cap, followed by Ethereum, at 17.1%. As more people have made (and lost) money in Cryptoassets, the number of explainers, books, podcasts, and “experts” has also exploded.

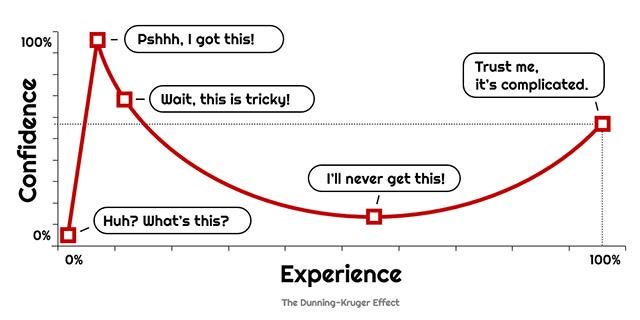

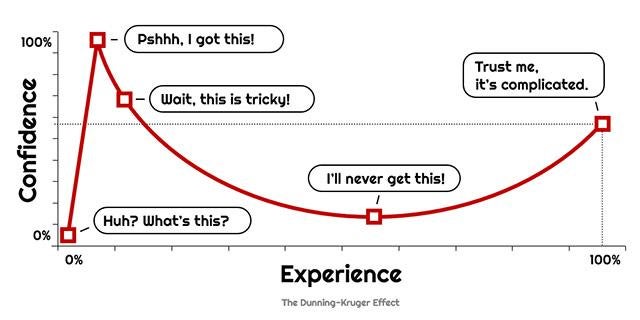

The problem with acquiring knowledge is that we tend to think we know more than we actually do. With that perceived knowledge comes overconfidence. This is known as the Dunning Kruger Effect (chart below.)

We would encourage investors to pair the amount they would invest (in any asset) with their knowledge and experience with that investment. In the world of real estate, watching a Youtube video or HGTV house-flipping show won’t prepare you to put a large portion of your net worth at risk in an investment property. You would want to meet with investors who have gone before you, possibly start with a small investment, lean on a Realtor for guidance, and maybe hire a property management company. The same goes for Cryptoassets. We need to be mindful of the difference between comfortability and confidence versus knowledge and experience.

If Bitcoin and other Cryptoassets have just been headlines or rumors for you and you want to expand your knowledge, here are some resources I have enjoyed:

- Books:

- Cryptoassets: The Innovative Investor’s Guide to Bitcoin and Beyond by Chris Burniske and Jack Tatar. I enjoyed this book for the clear explanations and “build your knowledge” approach. Since the authors knew the Cryptoasset market would evolve, they were intentional about writing evergreen content that would be helpful even today. And because it was released in late 2017, it is also fascinating to see how those Cryptoassets have evolved in the past four years (which is like decades in this space.)

- Cryptoassets: The Guide to Bitcoin, Blockchain, and Cryptocurrency For Investment Professionals This 64-page white paper written by the CFA Institute reads more like a small book. CFAI takes a measured approach exploring the addition of Cryptoassets to traditional portfolios.

- Podcast:

- Unchained hosted by Laura Shin, a former Forbes senior editor. This podcast started in 2016 and hosts some of the greatest minds in Crypto (all of whom seem to be on the right side of the Dunning Kruger chart.) Shin has a few episodes in particular that are helpful for beginners (Blockchain 101 With Andreas Antonopoulos, Answers to the Most Basic Crypto Questions, and Why Nothing is More Viral Than a Store of Value.)

- Online:

- Cryptopedia by Gemini contains great bite-sized explainers on all things crypto, for instance: What is Bitcoin in 5 Minutes.

- Coindesk provides primers along with how-to articles that get into buying, trading, storage, and staking. I found their individual breakdowns of different Cryptoassets particularly helpful.

Why Do I Want to Invest in Cryptoassets?

We have a tradition on our camping trips. At our first gas station stop, I buy 5 $1 lottery tickets (one for each family member.) If we win, the kids get to spend it on candy, and if we lose: “no candy for you!” Even though they could pocket their $1, no one wants to risk missing out on the big candy payout. On our last trip, we hit it big with $12 of Chewy Spree, Mike and Ike, Reece’s Pieces, and Starburst, minus the cost of future cavities.

We don’t buy lottery tickets to strike it rich, we’re doing it for the experience. And my kids choose to participate rather than keep their $1 because they want to avoid the regret of missing out on the big payday and the fun of playing along.

Many investors want to buy Cryptoassets for these behavioral reasons (“I want to be part of something” or “I don’t want to miss out.”) However, other investors’ primary motivation is financial (“I want a quick return” or “I need to own this as an emerging, legitimate asset class.”)

We saw a convergence of all of these motivations back in November of 2017 when Bitcoin was the hot topic at Thanksgiving tables everywhere. Aunts and Uncles heard tales of 1,000% returns in less than a year. ($90 invested in November of 2016 would have been $1,000 in November 2017). The desire to make up some lost retirement savings ground, make an “easy” dollar, or simply be part of the conversation turned many people into Cryptoasset owners over the 2017 Holidays.

Does Crypto Fit in My Investment Allocation and Financial Plan?

The measure of volatility in Cryptocurrency can be hard to get one’s head around. To carry our Thanksgiving example forward, just one year later in 2018, at the same Thanksgiving table, those same Aunts and Uncles were probably giving their nieces and nephews an earful. If Aunt Mae had decided to buy $5,000 of Bitcoin at Thanksgiving of 2017, she would only have $2,500 12 months later, after Bitcoin had fallen 50%.

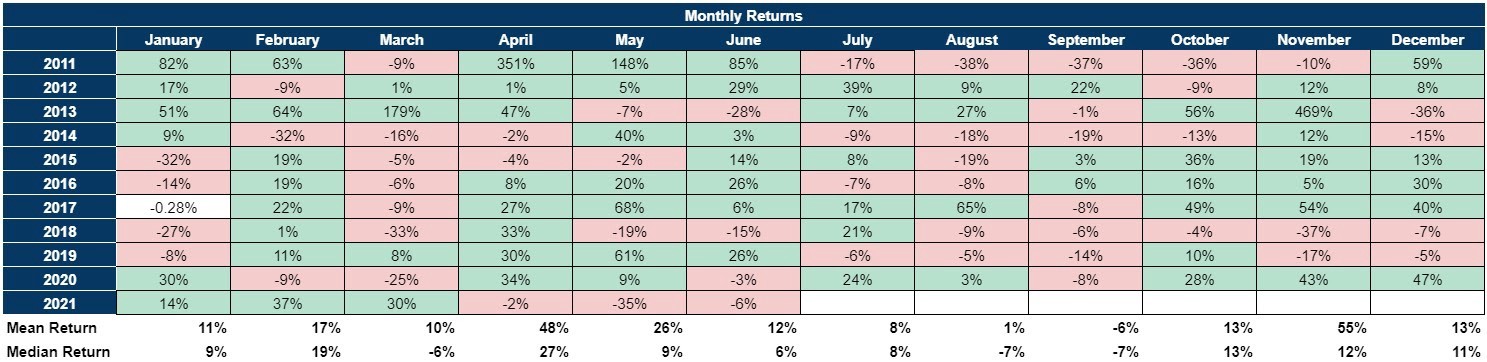

Whatever someone’s motivation for investing, it would have been hard to stomach those kinds of losses. But the wild ride wasn’t over. If Aunt Mae had the good fortune of missing the second Thanksgiving (2018) and the double fortune of forgetting about her Bitcoin investment altogether, her 50% loss would have been erased because her $2,500 account balance would have grown to roughly $38,000 as of April of 2021. But her roller coaster hasn’t stopped yet; Bitcoin has fallen another 50% in just the last three months, making Aunt Mae’s original investment of $5,000 worth just $19,000 at the time of this writing (assuming she never touched it.) The chart below details monthly (!) Bitcoin returns.

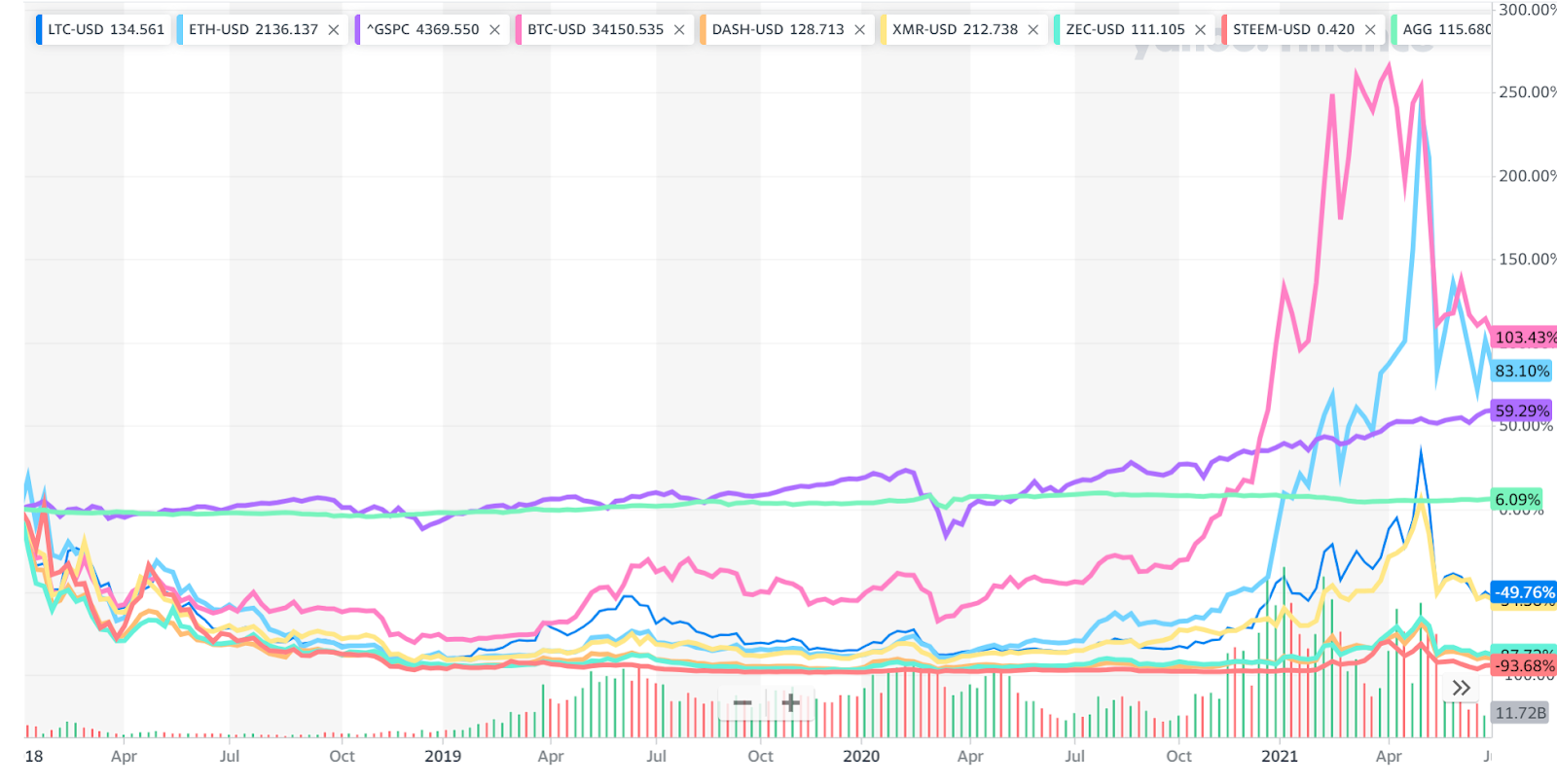

In the chart below, you’ll see some of the most popular and promising Cryptoassets when the book Cryptoassets debuted in October 2017 (which was, coincidentally, the month before that “first ” Thanksgiving in our examples above.)

We also plotted the S&P 500 (Purple) and Aggregate Bonds (Light Green) to show some reference. When an asset class, like Crypto, makes the S&P 500 look like a bond fund, you can begin to grasp the massive volatility in Cryptoassets.

Furthermore, we’ve found that the causes of an investment’s volatility (and an investor’s understanding and comfort with those causes) directly correlate to an investor’s ability to withstand that volatility. For example, when COVID-19 broke out, many stock and bond investors held firm based on a long history of investment markets, a tangible reason for the drop (the Pandemic), and the reasonable hope for sufficient financial and medical intervention.

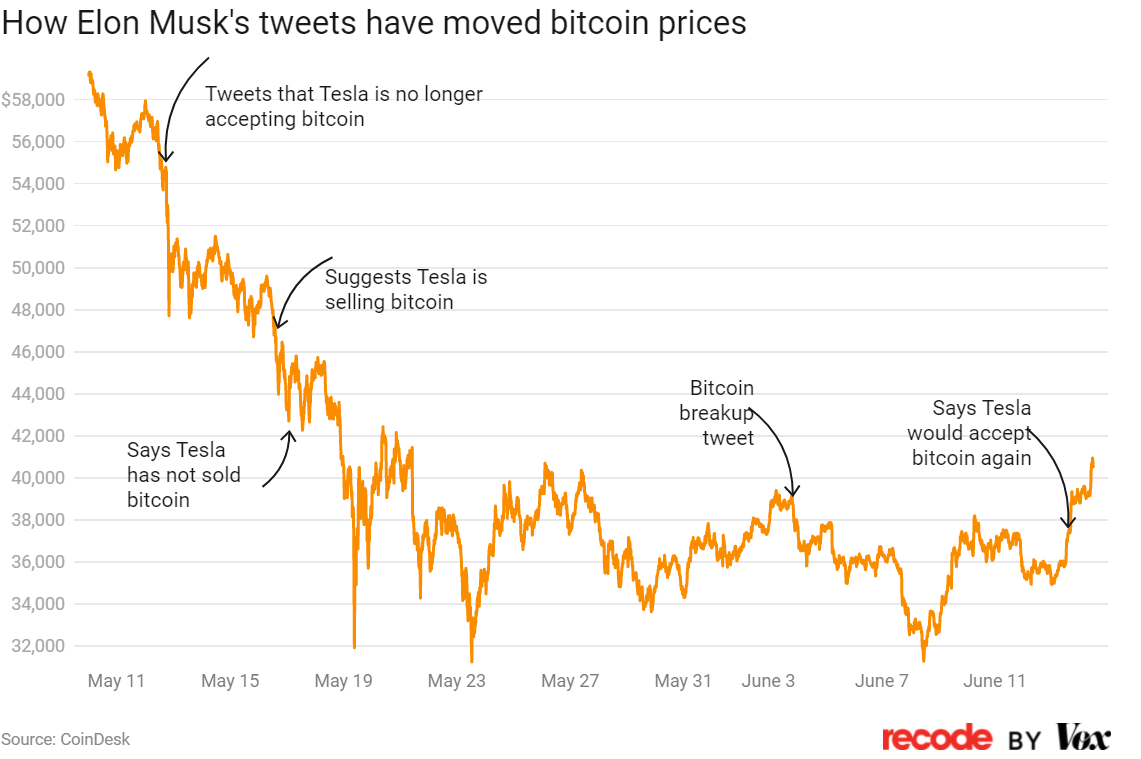

But at the current stage of Cryptoassets, volatility is exceptionally high and can come from all directions, ranging from SEC enforcement to Elon Musk’s tweets. Those swings can be harder to stomach because Cryptoasset investors (especially new ones) are in sparsely charted waters.

When the underlying asset is complex, volatility is high, and the source of that volatility is (at least on the surface) illogical and unpredictable, wise investors need to consider their complete financial plan and goals before deciding how much money (if any) they should allocate to Cryptoassets.

Since time and patience are an investor’s best friends, we know that the best investment plan is the one that keeps someone invested for the long term – in the words of Charlie Munger, “The first rule of compounding is to never interrupt it unnecessarily.” Investors need to make sure their allocation to volatile investments is low enough not to cause their overall plan irreparable harm. That allocation amount should come after carefully considering your “stomach” for risk (“how does it feel to experience this downturn?”) and your “wallet” for risk (“can my financial plan afford to experience this downturn?”) If you would like help in thinking through if and how Cryptoassets fit into your financial plan, we’d be happy to talk with you.

Justin Smith

Latest posts by Justin Smith (see all)

- Tariffs and a Declaration of Parental Independence - April 11, 2025

- Quarter in Charts – Q1 2025 - April 11, 2025

- Quarter in Charts – Q4 2024 - January 22, 2025