I Bonds Are Paying 9.62%, What’s The Catch? (Updated)

(Note: At the time of publication, July 2022, I Bonds were paying an annualized rate of 9.62%. Since then, interest rates and inflation have changed, causing the combined I Bond rate to adjust down to 6.89% as of February 2023. You can find the current combined interest rate here.)

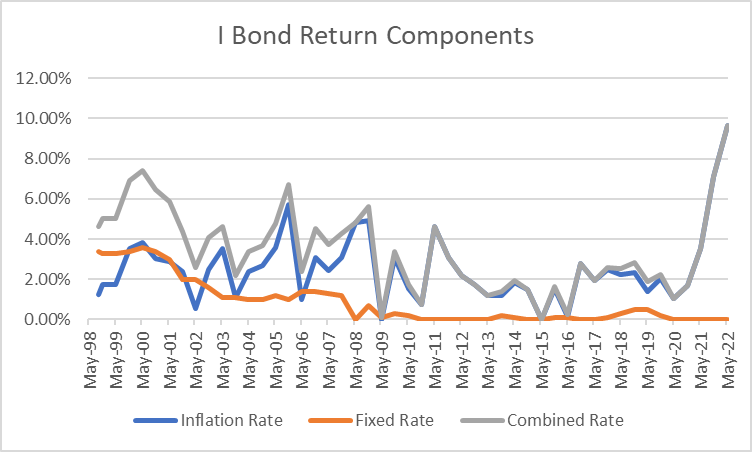

The US Government introduced Series I Bonds (the “i” is for inflation protection) in 1998 as a way for individuals to protect their savings and keep up with inflation. Until recently, most investors didn’t have much incentive to pay attention to I Bonds. They are cumbersome to purchase, limited in denomination, and have certain restrictions. But since the Treasury announced a 7.12% annualized rate in November 2021 and, more recently, a 9.62% annualized rate announced in May 2022, investors should consider giving I Bonds a place at the table.

Rate of Return = Fixed Rate + Inflation Rate

I Bond returns combine two rates of return: the Fixed Rate and the Inflation Rate.

The Fixed Rate component is tied to prevailing interest rates at the time of purchase. This rate is fixed for the entire time that an investor holds an I Bond (up to 30 years.) The current Fixed Rate is set at 0.00% and has averaged 0.90% since I Bonds were introduced in 1998.

The Inflation Rate component is tied to inflation and is adjusted every six months, in May and November. The current Inflation Rate for I Bonds is 9.62% annualized.) The Inflation Rate component has fluctuated from -5.56% to the current 9.62%%. However, since I Bonds cap the Inflation Rate at 0% (it can’t have a negative rate of return), the actual Inflation Rate has ranged from 0% to 9.62%%, with an average of 2.54% annualized.

An investor who buys I Bonds today will earn 0% on the Fixed Rate side (for the next 30 years or as long as they own it), but will also currently earn a variable Inflation Rate return, set at 9.62% (as of May 2022) annualized for the first six months. Then, six months after purchase, the inflation rate will reset to the newest rate (annouced in November and May.)

Alternatively, the investor who bought I Bonds in May 2000 (when the fixed rate was 3.60%), will always earn 3.60% more than an investor who buys I Bonds today when the fixed rate is 0%.

Advantages

- Rate of Return – There is plenty that is attractive about I Bonds, but the main appeal is the rate of return compared to traditional CDs, money market funds, and savings accounts. Earning 9.62% annualized until November 2022 (even if the Inflation Rate resets much lower at that point) is a far better return than the going rates with traditional banking options.

- Protection of Principal – I Bonds are backed by the US Government and are not marketable on the secondary markets. This means that the US Government is the only buyer and seller, thus creating stability in the price. If I buy $1,000 of I Bonds, I will always get $1,000 (plus my earned interest) as long as the government doesn’t default on its promise.

- Elimination of Interest Rate Risk – Typically, when interest rates rise, bond prices fall. This is because holders of older, lower interest rate bonds need to drop their “sale” price to compete with newer, higher interest bonds. This dynamic has created poor returns for the bond market so far in 2022. I Bonds don’t have the same relationship to rising interest rates because they sell for par value and are redeemed for the same par value.

- Tax Deferral – The default option for I Bonds is to pay the tax upon redemption. If I redeem my I Bonds while working, I’ll pay federal tax, but no state or local tax, on the interest at my highest marginal tax rate (just like I would for any CD or Money Market fund.) But if I wait to redeem them when my income is lower, I could enjoy a lower tax rate.

- Tax Avoidance (for College) – I Bonds can potentially be a great tool to pay for qualified higher education expenses, but there are some stipulations. While parents are allowed to buy I Bonds in their child’s name (more on that below,) those I Bonds wouldn’t be exempt from taxes if used for education. I Bonds must be purchased in the parent’s name to be eligible for any potential tax savings. Additionally, if a parent’s modified adjusted gross income is above certain limits ($98,200 for single or $154,800 if married filing jointly in 2022), their I Bonds would not be exempt from taxes. If parents file Married Filing Separately, they are excluded from the tax exemption regardless of income. More information on education planning and I Bonds here.

Limitations

- Access to Funds – I Bonds cannot be redeemed within the first 12 months of purchase (barring a federally declared disaster.) If an investor redeems their I Bonds after 12 months, but before 5 years, they will forfeit the last 3 months of interest (similar to redeeming a CD early.) After 5 years, I Bond investors can redeem without giving up any interest.

- Dollar Limit – In simplest terms, the Treasury limits each individual to $10,000 of I Bonds per calendar year. Investors can purchase additional paper I Bonds if they are do a Federal refund (limited to $5,000 or the amount of the refund, whichever is smaller.) Parents (or Grandparents) can buy I Bonds in their offspring’s name (or give them as a gift) but must be mindful of how they are taxed (and limitations if they intend to use them for education.) If investors want to get creative, they can purchase I Bonds in the name of trusts, estates, partnerships and/or businesses. However, once investors get into this area, it would be wise to seek counsel on making sure the trusts or entities are set up correctly, and the purchases are within the code. The “return on hassle” might not be worth it.

- Ease of Purchase – Sadly, I Bonds are unavailable through traditional custodians or 401k plans. Investors can only purchase them directly from the US Treasury. The easiest method is online at TreasuryDirect.gov, but “easy” would be a stretch. It took me about 20 minutes to establish my account, link it to my bank account, and make my purchase. Each time I log in, I am emailed a new “one-time” password and must also click on the on-screen virtual keyboard to enter my personal password. Each investor will need to assess if the return is worth their effort.

- Rate of Return – While “rate of return” is in our list of Advantages (above), it is also in our list of Limitations. That is because I Bonds can be attractive compared to CDs and Money Market funds, but they have historically been disappointing compared to Bond and Equity returns. The chart below highlights the real returns (returns above inflation) for bonds (dark green) and stocks (light green.) For the last 120 years, any time the green boxes are above the 0 horizontal line, their returns would outpace inflation (or I Bonds.) For stocks, that would be 95% of the time; for bonds that would be 80% of the time. Only in a prolonged extreme inflation scenario would I Bonds have outperformed stock and bonds (if I Bonds had been around since 1900.) While that may be the situation we’re in, we would still encourage investors to compare I Bonds to other short-term savings vehicles rather than stocks and bonds.

SPWM does not hold I bonds for our clients at the time of this blog and we are only providing this article for educational purposes. It is not intended to provide specific advice or recommendations for any individual.

For further disclosures, please see this link.

Justin Smith

Latest posts by Justin Smith (see all)

- Tariffs and a Declaration of Parental Independence - April 11, 2025

- Quarter in Charts – Q1 2025 - April 11, 2025

- Quarter in Charts – Q4 2024 - January 22, 2025