Quarter in Charts – Q2 2022

“The Circumstances”

So far this year, investors have experienced a dramatic increase in interest rates and sustained high inflation, coupled with a decrease in both stock and bond prices not seen in half a century. All of this while the US continued to add jobs and public companies increased profits at a steady pace. Below we will walk through “the circumstances” and how they relate to investors.

Inflation

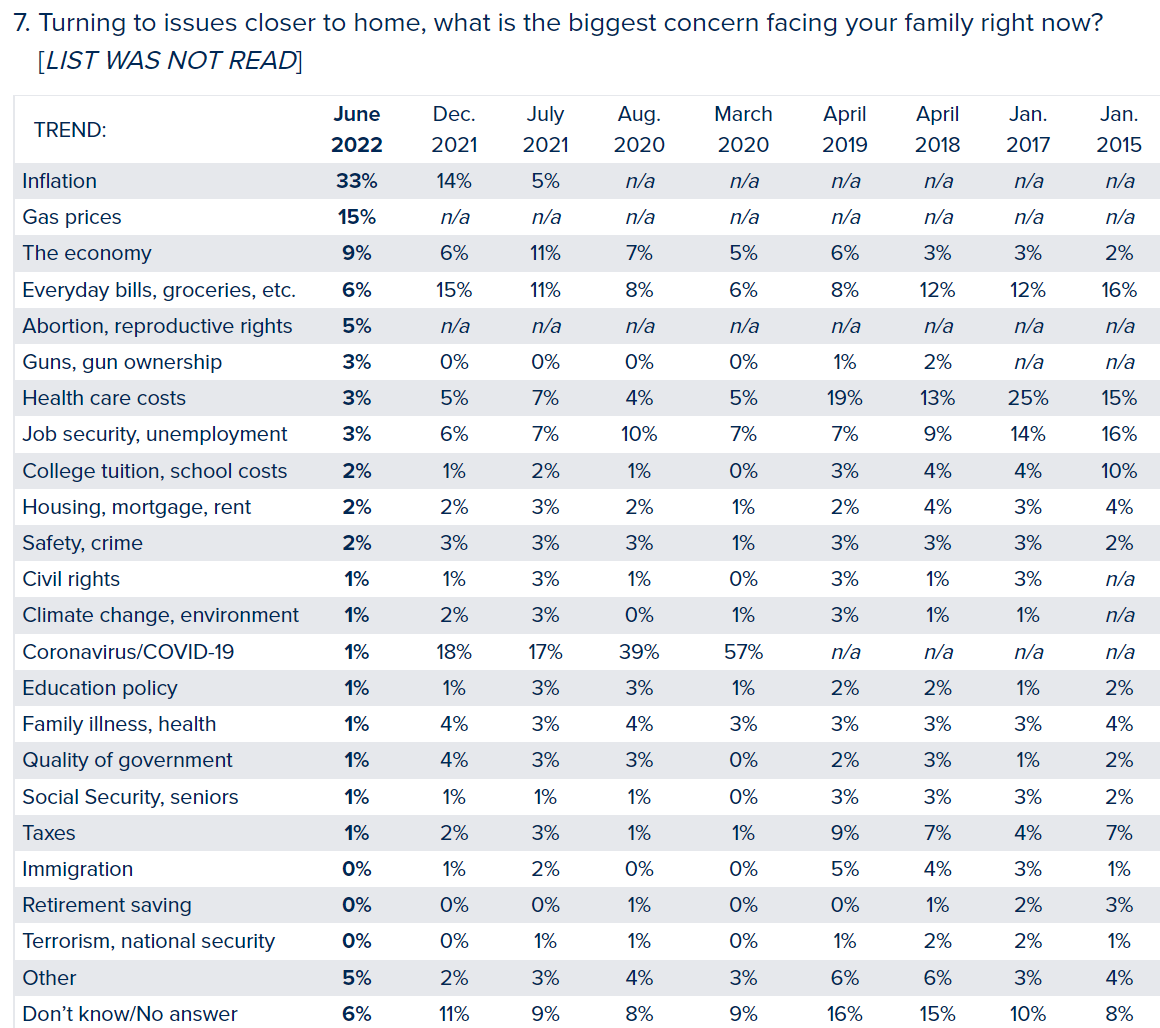

In a recent Monmouth University poll, when asked for “the biggest concern facing your family,” respondents overwhelmingly pointed to increasing prices. In the chart below, “inflation” and “gas prices” were the top concerns for 33% and 15% of respondents, respectively. You could make the case that “everyday bills, groceries”, “healthcare costs”, “school costs” and “housing” are all top concerns because of the rising cost of those items.

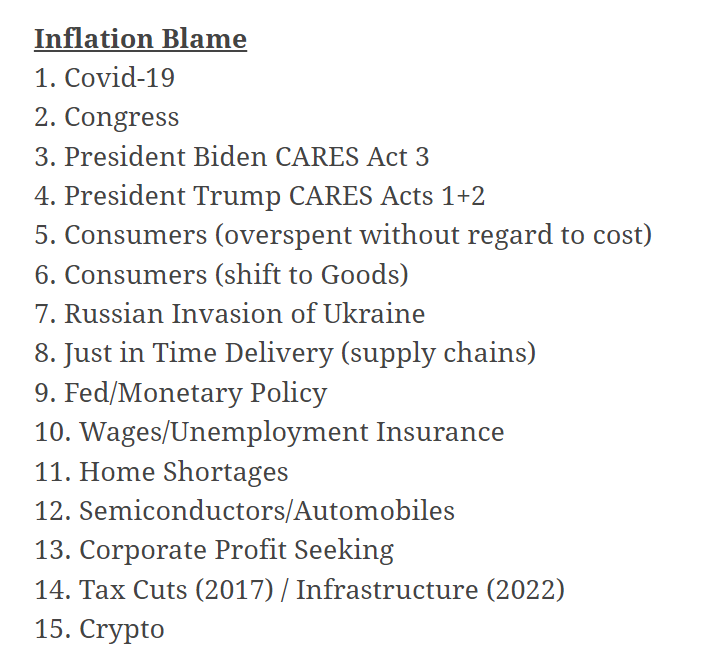

As a parent of three kids (9, 12, and 14), I’ve mediated plenty of fights and have said “I don’t care who started it” more times than I care to mention. Regarding our current inflation problem, I enjoyed Barry Ritholtz’s breakdown below (and detailed linked blog post) of “who started it.”

It is helpful to see the “sources” of inflation as a directional pointer to whether inflation will stick around or be temporary (or some combination.) For example, if “semiconductors/automobiles” was the primary reason, then an eventual solution to that issue would bring down inflation. However, the source of inflation runs much deeper.

Further, it is worth noting that “who started it” probably isn’t who can end it. Rather, we’ll likely have to continue to depend on the Fed to act as the parent here, cleaning up the mess. The overwhelming consensus is that the Fed hasn’t moved quickly or comprehensively enough in that effort.

Recession Possibilities

While overall economic output is down (a vital component of a technical recession), corporate profit margins are high, unemployment is extremely low, and companies and consumers have more cash reserves than ever. So if we go into a recession, what could that look like for business owners, consumers, and investors?

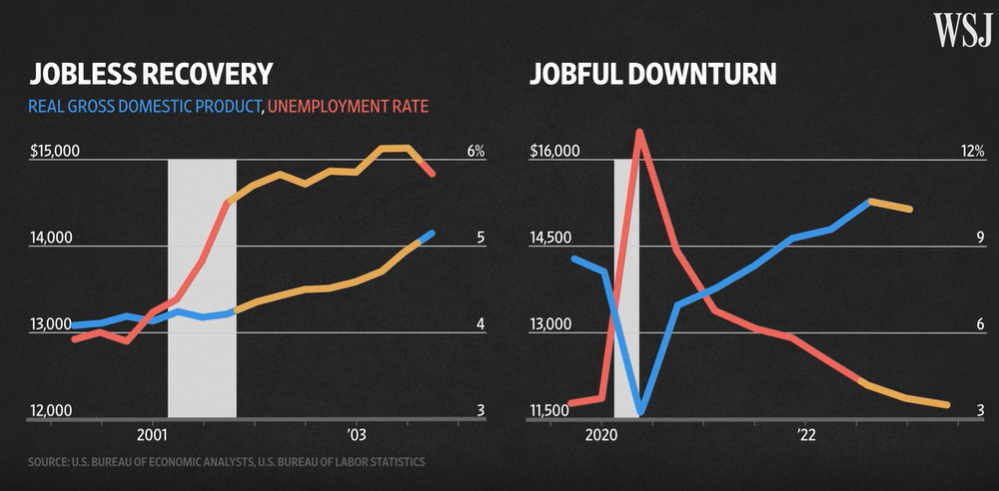

The Wall Street Journal has produced an extremely informative 5-minute video explaining the current (potential) recession and job market compared to previous recessions. They labeled the likely situation as a “Jobful Downturn” (as opposed to a “Jobless Recovery”) and much of the impact depends on how businesses decide to proceed. Do they cut employees (that they just fought tooth and nail to hire), or do they cut into (record high) profit margins and cash reserves? A company with long-term prospects and focus will likely do the latter, which could cut the recession short.

US Stock and Bond Returns

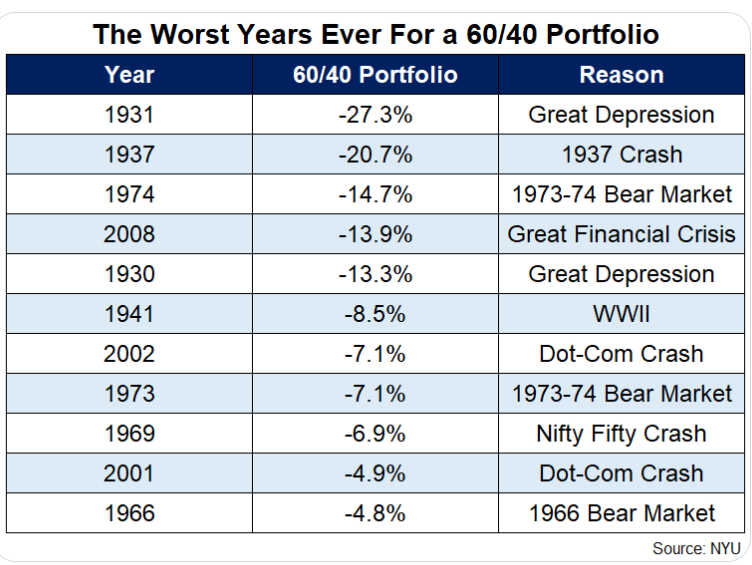

Typically we look at US Stock and Bond returns separately. However, they have taken such an unprecedented move downward together that we’ll start there. In a recent blog post, Ben Carlson shows that over the last 94 years, a 60/40 portfolio (60% S&P 500 stocks and 40% US Aggregate bonds) has had some bad years (below.) But if we ended 2022 now (and some folks wish we could), the 60/40 year-to-date return of -13% would rank as the 6th worst year ever for the balanced portfolio.

Where Are the Outliers?

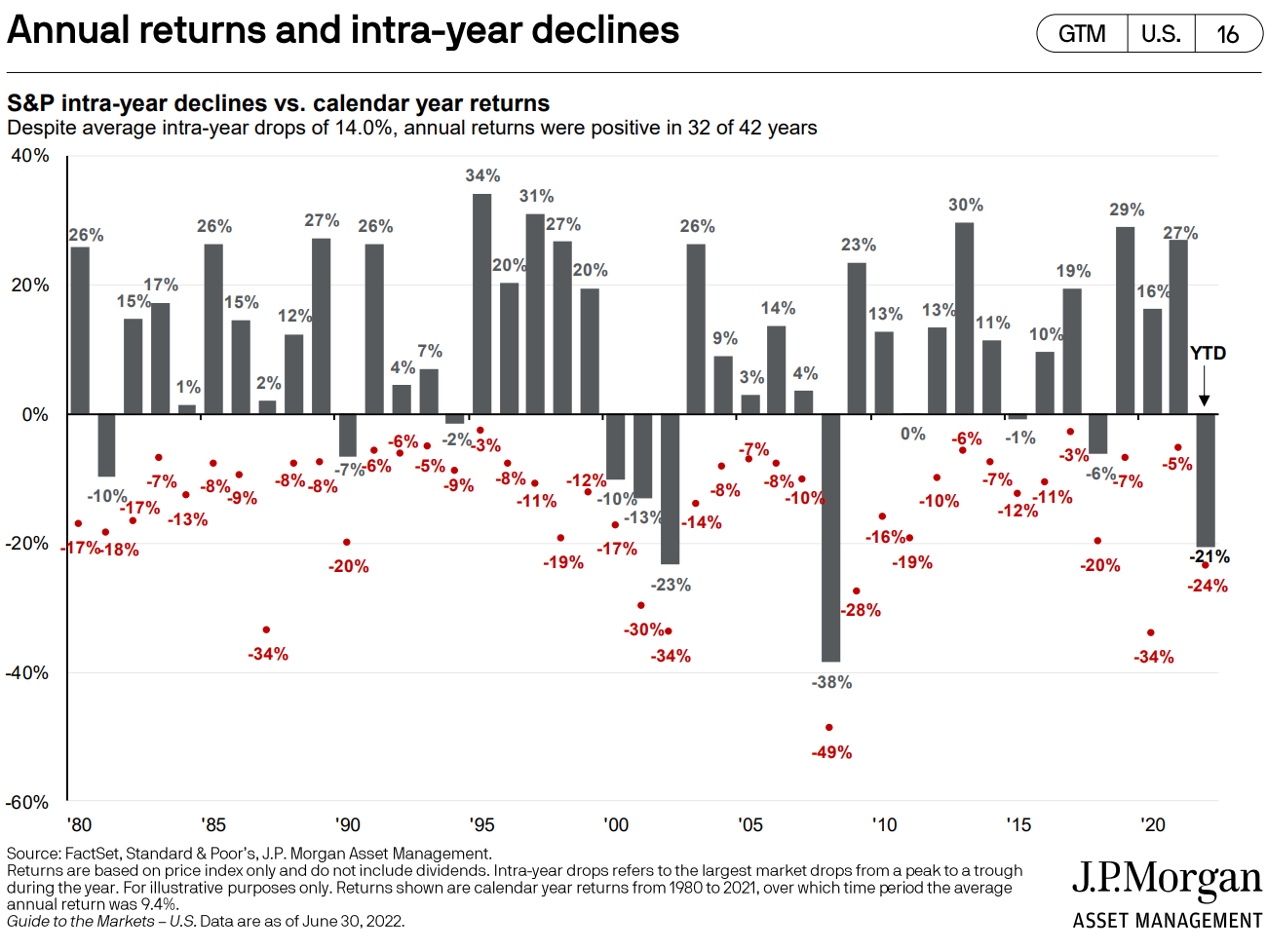

US Stock returns have been hit hard, with the S&P 500 ending the first half of the year down 21%. As the chart below shows, the average S&P 500 intra-year decline over the last 42 years has been -14%. More than 1/4 of the years have experienced declines of -19% or more. So while the decline year to date hurts, we certainly shouldn’t see it as a rare event.

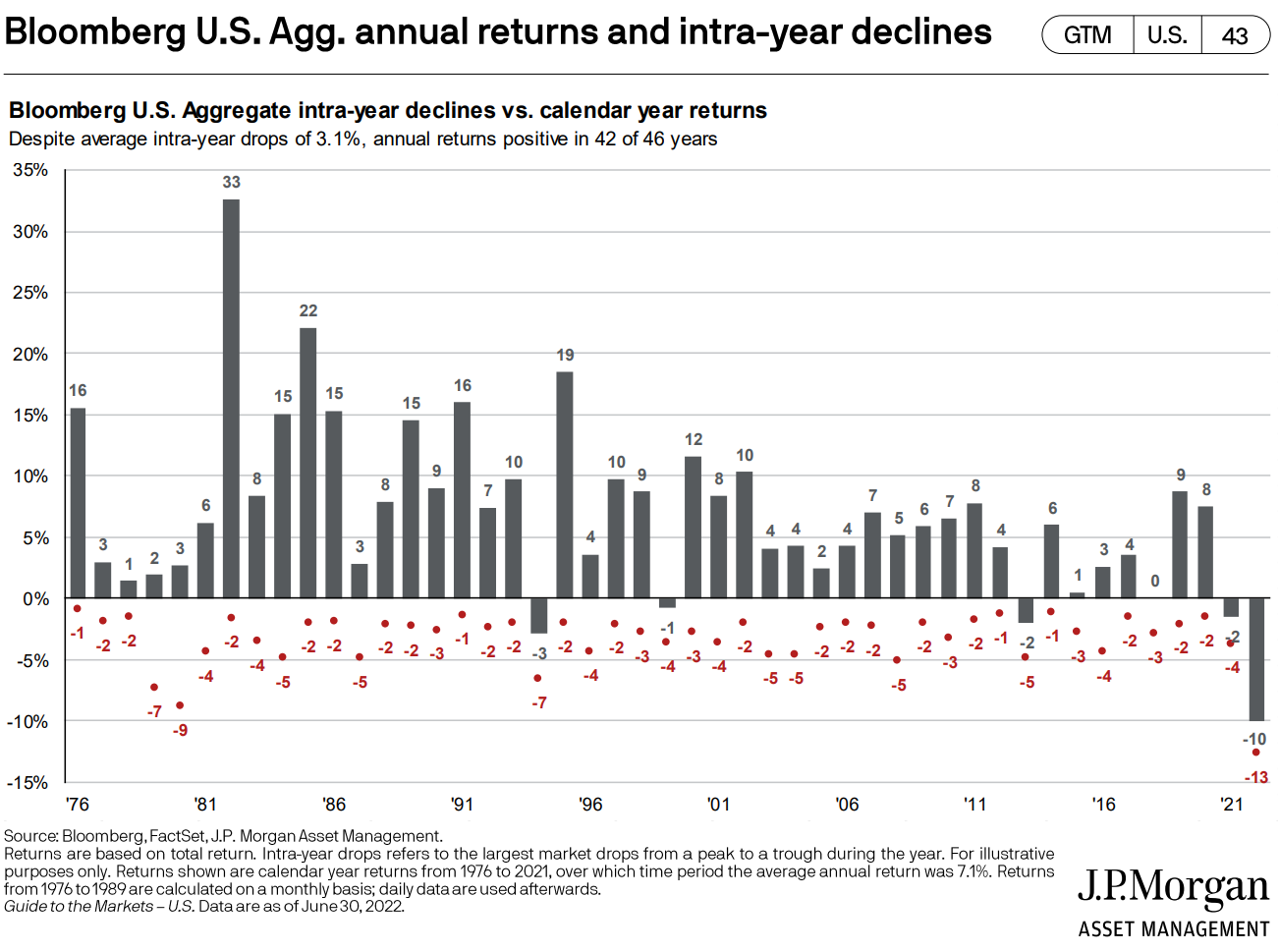

Bonds, on the other hand, have experienced a very rare year to date. With interest rates increasing dramatically from a low starting point, the Bloomberg US Aggregate bond index had its largest intra-year decline since its inception (below).

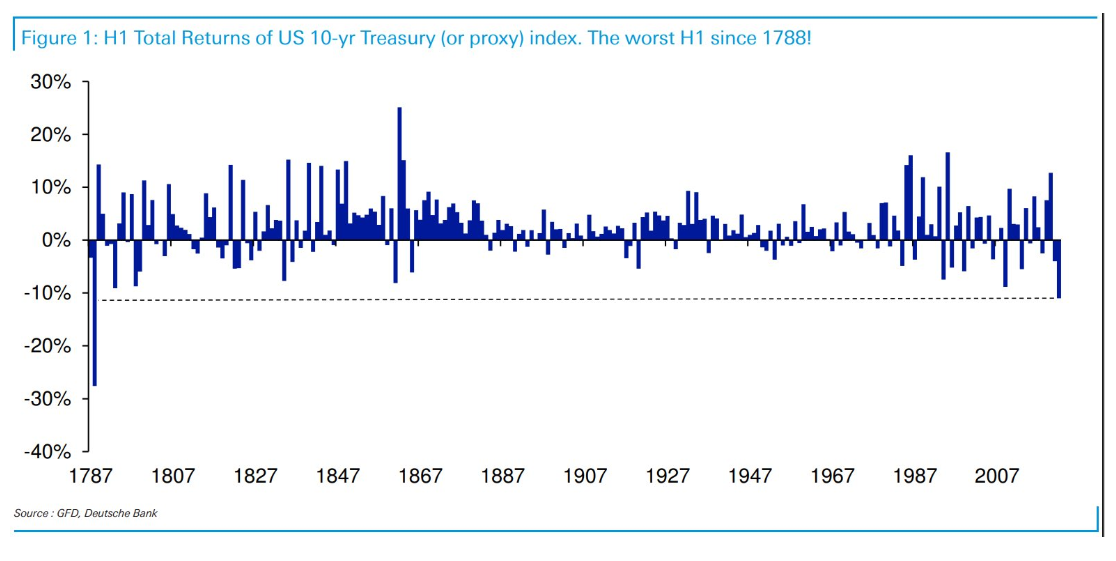

If we get in a time machine and look at just 10-year US Treasuries, we would have to go back centuries to find a worse first half of the year for these “safe” instruments (see Michael Batnick’s post.)

Maybe I Should Quit While I’m Ahead?

I heard the following lyrics through my headphones while mowing my lawn the other week, and it made me think of how most investors probably feel:

“And I am busted, broken, bent, and beaten ’bout halfway to dead…

Well maybe I should quit while I’m ahead, oh Lord.

Maybe I should quit while I’m ahead”

Turnpike Troubadours

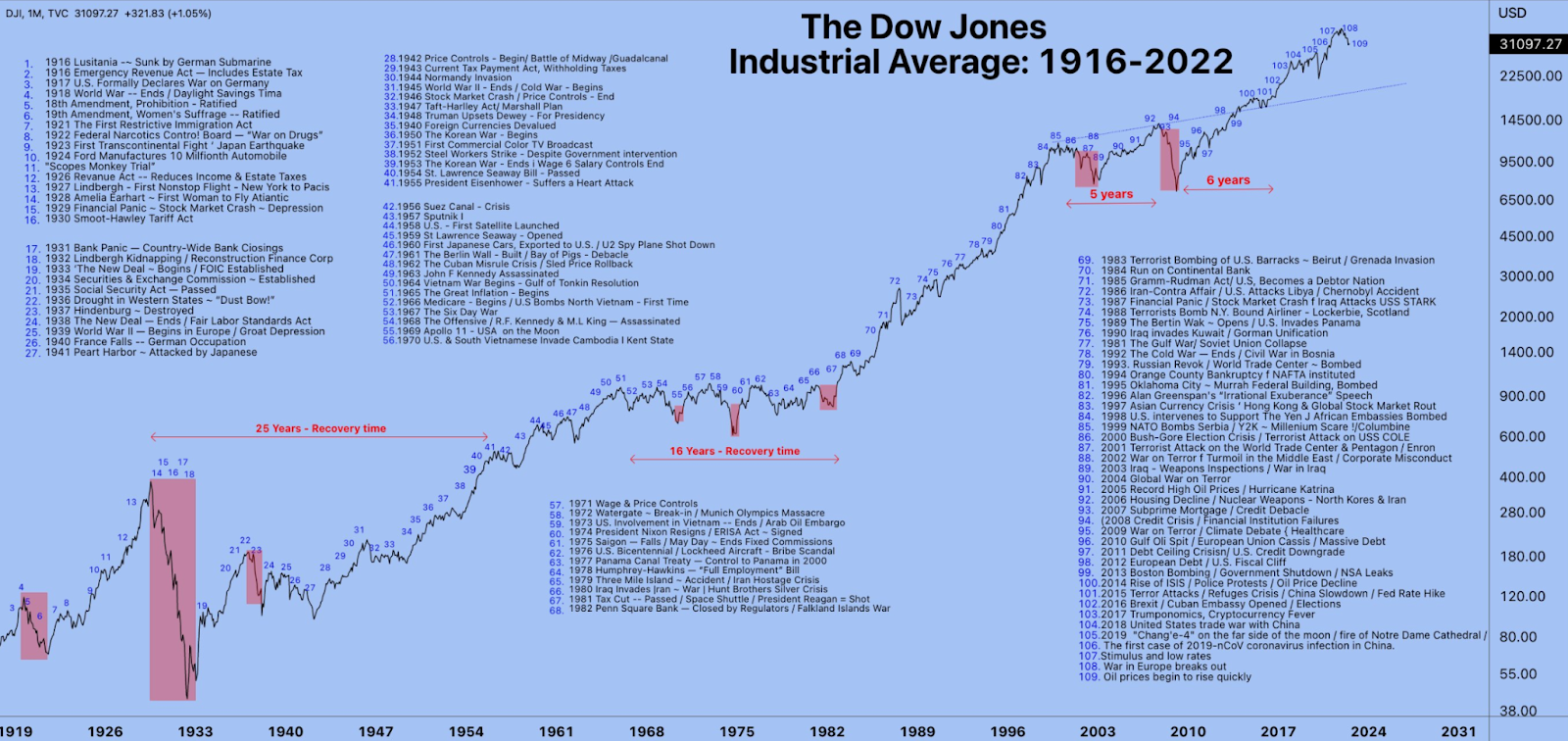

History shows us that we need to be prepared to be “busted, broken, bent, and beaten” by financial markets because it happens a lot (chart below.) The potential to feel (as the Turnpike Troubadours put it) “’bout halfway to dead” at any moment might feel like a detour from potential good investment returns. But it is also the reason for potential good investment returns. If stock and bond markets could never fall from their highs, they would be called money market funds and they would carry the same risk-appropriate returns.

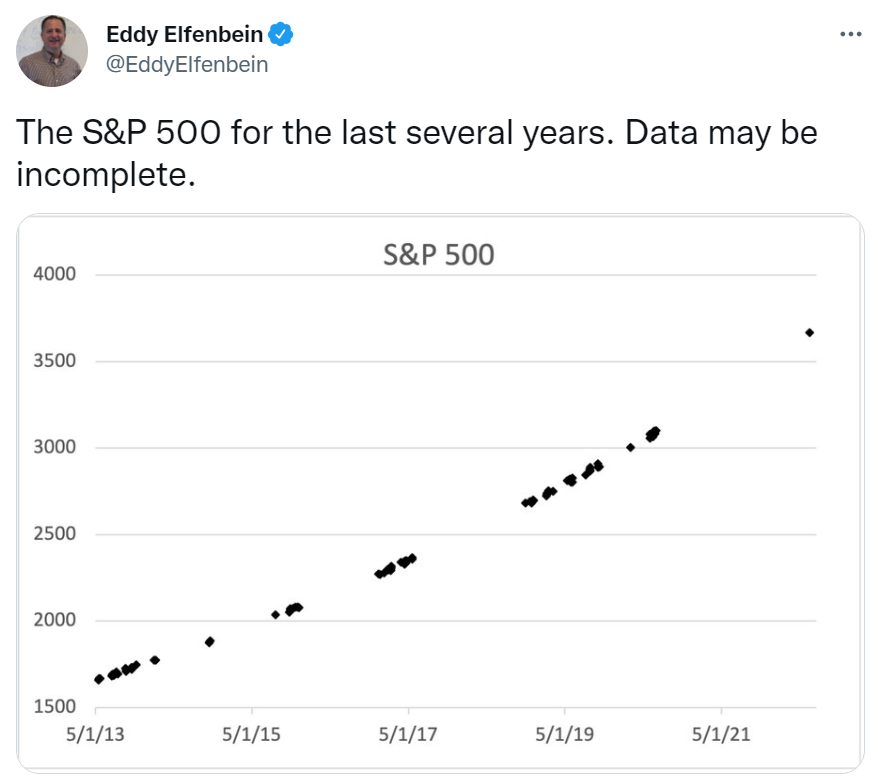

If the above chart is still daunting, you may prefer the one below. Eddy Elfenbein periodically updates the following chart with a (tongue in cheek) disclosure: “data may be incomplete.” While Eddy is obviously taking “white out” to the variability of investment returns, this chart should ring true for many investors, even those already in retirement.

A retiree withdrawing 4-5% per year from their investment accounts, could have the ability to ignore the noise for the vast majority of their assets. Furthermore, if that investor is proactively planning for reasonable withdrawals through cash reserves, dividend yields, and short-term bonds funds, they may have the mental and financial flexibility to “white out” even more years.

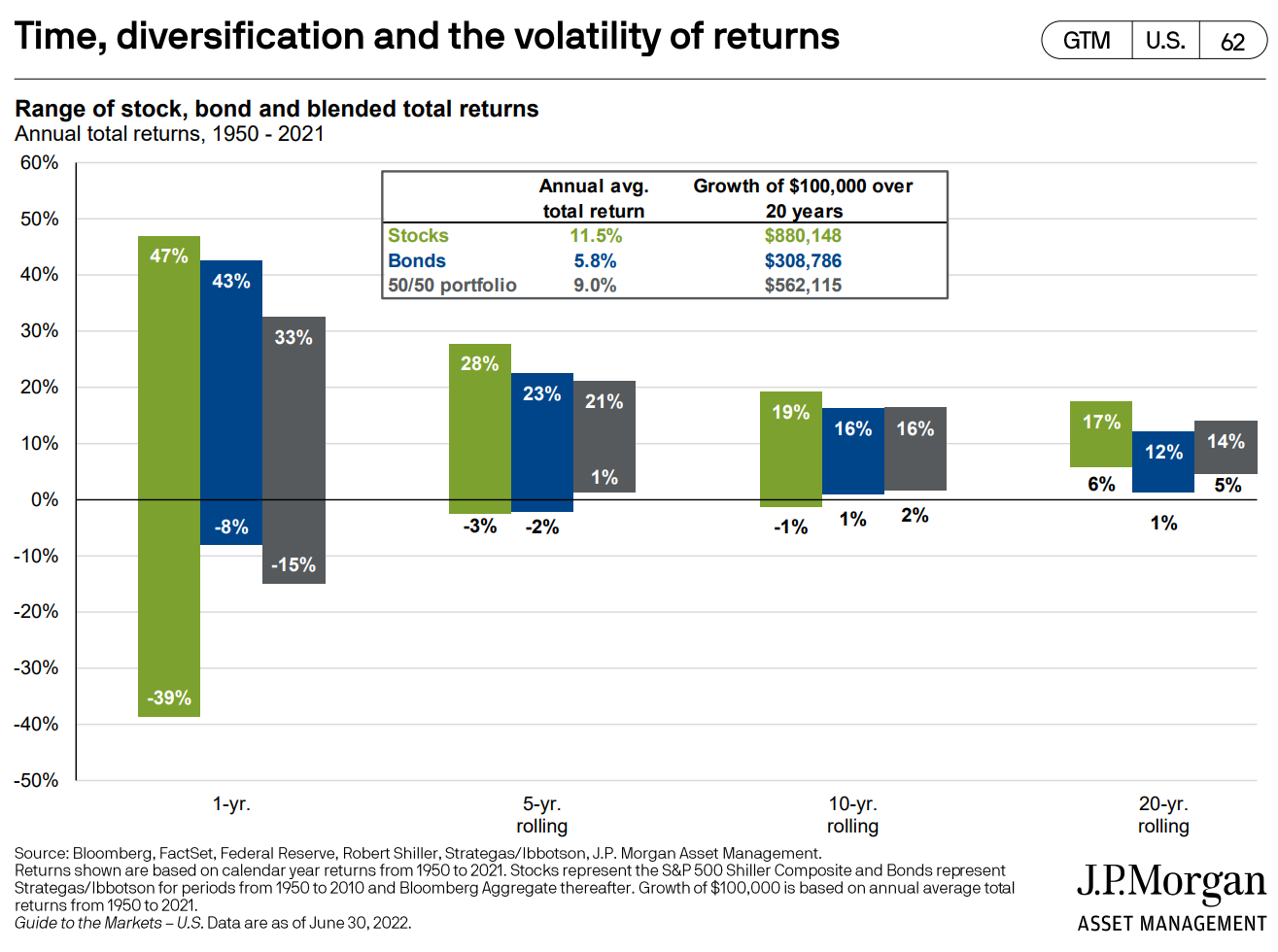

We think it is helpful to consider investment dollars in terms of their timeline. The chart below shows the band of outcomes for US Stocks, Bonds, and a 50/50 portfolio over 1, 5, 10, and 20-year periods. In the short term, stock and bond returns have been highly variable (and as we noted above, if 2022 ended today, the bottom edge of the blue bar would drop to -13% in the 1 yr portion of the chart.) However, the vast majority of the average investor’s dollars will not be spent in the next year (if they are, then they shouldn’t be invested in the first place.) Rather, the lifetime of most dollars is 5, 10, or 20+ years out.

The Turnpike Troubadours singer points out that he is in a bad spot now and wonders if he might still have further to fall. The same is always true for investors in a downturn. Just as we have notched a new “belt loop” for the downside of bonds this year, we could always be entering into a new “worst” season for stocks and balanced allocations. What would that look like?

Let’s assume a 50/50 portfolio investor notches a -16% annual return for 2022. In order to match the worst 5-year return since 1950, they would need to earn an average annual return of +1% throughout the entire five years (chart above, 5-year rolling group, bottom edge of the gray bar.) So after earning -16% in the first year, that investor would need to earn +5.77% each year for the next four years to end up with +1% average annual returns over the half-decade. While investors wouldn’t welcome the first year, it would be hard to justify “quitting while I’m ahead.”

It is helpful to remember that every market downturn feels like a risk while we are in it, but it feels like an opportunity when we look back on it. The key is to take the most prudent actions (or inactions) while in it, so that we’re still on track for our goals when we’re eventually on the other side of it.

For further disclosures, please see this link.

Justin Smith

Latest posts by Justin Smith (see all)

- Tariffs and a Declaration of Parental Independence - April 11, 2025

- Quarter in Charts – Q1 2025 - April 11, 2025

- Quarter in Charts – Q4 2024 - January 22, 2025