6 Financial Commandments for Twenty Somethings

For the last 5 years I’ve had the privilege of mentoring a few young men. And by mentor, I mean they are younger and more interesting than me so I tag along on their trips and we share life together (I’m talking about you Tice, Tom, and Pearce). I wanted to write a letter of financial advice to them for when they graduate from college; figured I’d let everyone else read along.

Post College Life

The first thing you will realize after graduation is that you will have more freedom along with more responsibility. God willing you will have jobs and move out of your parent’s house sooner rather than later. However, it’s not the end of the world if you travel for a year instead of going straight into business casual. With your new job you will have more income, but with your new residence, more bills. Where $400 used to last you a month, now it lasts a week. You know you should be doing something to prepare but don’t know exactly what. When this moment comes, you need to take a breath and think about this article I wrote you about your financial commandments.

Be Patient

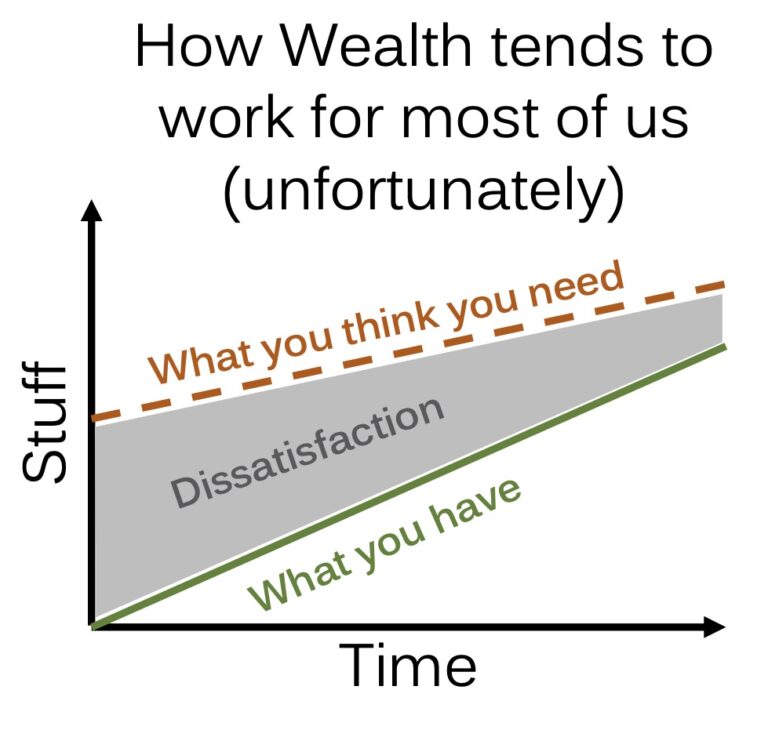

There’s a pattern that I’ve noticed in individuals who are successful. People who can control their short term urges and emotions in pursuit of a greater goal often end up making better decisions. You need to learn how things work, what’s worth buying and what isn’t, what’s a Roth IRA and what’s a budget? Through this learning process you are investing in yourself. The process of investing in yourself is more important than any car, mutual fund or account you can open. You should seek out designations, mentors and colleagues that push you and make you better at your job. What you do to prepare now will be magnified later. Despite how attractive money is, your decisions shouldn’t always be driven by dollars. Go where you can learn and grow into a more valuable employee. Becoming valuable will allow you to control your future, you will have more power in deciding where and how you want to live.

Make A Budget

You can call it a cash flow plan if it makes you feel sophisticated, but your budget should account for every dollar that comes in and goes out. One of the most important line items will be your savings. This “savings” word really means freedom. That little word can provide you with fun trips, a nice house, a car and much more! Don’t give it a measly 5% unless that’s the kind of trip, house or car that you want. You should save 10%-30% of your income. In order to have a 10%-30% savings number, it helps to keep your fixed expenses low. This looks like sharing rent with a roommate or two, buying a used car for around $5,000 and cooking food at home instead of eating chicken minis every day. One key part of this budget, to ensure you don’t become a scrooge, is to budget for fun (I’m sure Pearce won’t have a problem here). This life isn’t guaranteed and if you spend all your effort planning for when you’re 60 then “60 year old you” will be beyond frustrated with “25 year old you” for not collecting all of the fun memories he’s been hearing about. Go to the concert (with tickets that actually work –Tice) and buy the wakeboard (Tom) but save and plan for it. I’d also recommend giving away money and time, you can read more about that HERE.

Get Out Of Debt

Especially if this debt is tied to high interest rates or depreciating assets like a car. Most likely you will have student loan debt which I cover HERE. For a car and credit card, it almost always makes sense to pay off the highest interest rate first or use the debt snowball method. Once your debt is paid off, then fund a money market or savings account to cover 6 months of living expenses. This means you should have enough saved to pay for rent, food, insurance, and gas for 6 months. The reason for this account is to keep you out of debt when you hit a hard time later in life. Instead of racking up credit card debt to survive you can withdraw from your emergency fund.

Start Planning For Retirement

What?! But that’s literally 45 years away… I know, but you don’t want to have to rely on junior versions of yourselves when you’re 80. You want to feel assured that you did the right things early in life to prepare for your future and your future family. This means you need to look into your 401(k) options at work, is there a Roth option, do they match your contribution, should you open an HSA, etc. These are all questions you should ask and find the answers to before you start investing. I would suggest researching online blogs for education such as Mr. Money Moustache, Financial Ducks in a Row and Oblivious Investor. However, it helps to have a financially savvy friend (me), family member or financial advisor (also me) that you can bounce big decisions off of.

The reason you need to invest now is because your money has the longest amount of time to grow before retirement. Early investing allows you to magnify the effects of compounding interest. Einstein allegedly said that compound interest is the 8th wonder of the world. For instance, if your money grows at 7.2% per year then every 10 years it will double in value. Which means if Grandma gave you $50,000 today and you had 40 years until retirement, that money could become $800,000 without you adding a dime to it! Click HERE for a list of islands you could buy with that money. Of course, that also means that if you wait to start investing that money 10 years from now, then it will cut that number in half to $400,000, leaving you with no island…

Insurance

You need to have one question in mind when considering insurance. Can I afford to lose this? If you can’t afford to lose everything in your house then renters insurance is a good idea. Your most valuable asset after graduation is your future earnings potential. You can’t afford to lose your future earnings potential, therefore, you should purchase a long term disability insurance policy. If you don’t have any debt or a family then you don’t need life insurance, this seems obvious but trust me, people have made this mistake plenty of times. You should have health insurance which is most likely provided through work, if it isn’t, you can look up a cost effective provider by clicking HERE. Side note, you can mooch your parents’ health and dental insurance until you’re 26. Dental insurance often isn’t necessary as the cost to benefit is a wash and an HSA account can be used instead. On the whole, be patient before signing up for any insurance policies. You must read the fine print and price shop because you most likely won’t change your mind once a policy is selected. Small decisions here can save you a lot of money when it comes time to call in a claim.

Hang out with the right people

I know Whitney, Lou, and Lynne would agree with Tim Ferriss on this one, “You’re the average of the 5 people you spend the most time around.” This means that you probably like to do the same things as these individuals. You shop at similar stores, talk the same, go on trips together, eat the same food, and build comparable habits. Pick your friends, mentors and wives wisely because they will have a large impact on how you act financially.

Closing Time

These decisions are going to be hard, at first, but you will learn to love the process. It’s hard to drive a $5,000 car when all your friends are “buying” or leasing $40,000 cars, it’s hard to cook your own meals, and it’s hard to stick to a budget. However, these present day investments, financially and mentally, will be the foundation to your success 5, 10 and 20 years from now. Good decisions now will allow you to have less stress and, in turn, give you the clarity of mind to make intelligent key decisions later in life. Before making a large financial decision it is helpful to consider what Andy Stanley said best, “Based on my past experience, current circumstances and future hopes and dreams, what’s the wise thing for me to do.”

Stephen Boatman

Latest posts by Stephen Boatman (see all)

- How to Calculate and Maximize Your Social Security Benefit - May 19, 2023

- An Unaffordable Housing Market: Why and What’s Next? - March 14, 2023

- $500 Billion Student Loan Forgiveness Update ($10k/$20k, New IDR Plan, 0% Interest Ending) - October 20, 2022