How Much Car Can You Afford?

When you google this question, you get a few responses:

- What you can pay in cash

- No more than 35% of your income

- 20% down + payments that aren’t higher than 10% of your monthly income or

- “Tell me what you want your monthly payment to be?” (thank you, car dealers)

However, the answer isn’t the same for everyone. One person may have a large student loan, mortgage, auto loan, or credit card debt to manage, while another has savings built up, no debt, and already spends less than they make. Or they may be married with kids, and the other is single, you get the picture. With all of these variables, how can we decide how much car we can afford?

We will solve this problem using a sliding scale. Our scale will range from 10% to 30% of our annual pre-tax income. And note that the 10% to 30% number is our household’s car value, not the amount we should pay for each car.

10% → 20% → 30%

10% example: $80,000 earned, $8,000 car purchase price

30% example: $80,000 earned $24,000 car purchase price

A person should lean towards the 10% limit if they:

- Have consistent credit card debt that is producing an interest charge

- See a car as a tool to get from point A to point B

- Value travel, home, vacation home, experiences, etc. more than their car

- Owe student loan debt equal to 100% or more than their income

- Earn a household income below $80k

- Save less than 10% of their after-tax income for retirement.

- Struggle to afford primary medical care (annual check-up and dental visits)

- Don’t have six months of living expenses in an emergency fund

You could lean towards the 30% limit if they:

- Have no debt (Exception: a mortgage that costs less than 30% of take-home pay)

- Earn an income of over $80,000

- Save above 15% of their after-tax income

- Generally experience a financially stress-free life

- Enjoy talking about their car with friends/family

- Live well below their means

- Have six months of living expenses in an emergency fund

The above variables should tell you how much you can get away with spending. But there are other essential variables to consider when it comes to purchasing a car. Such as car turnover/time of ownership, should you finance or pay with cash, and how new of a car should you buy?

Car Turnover

No, this doesn’t refer to the Reliant Robin who rolls over with a 15mph corner. By turnover, we mean how frequently you buy a new car. Driving a car for 10+ years lowers three large expenses, depreciation, car insurance, and (hopefully) getting out of a car payment to free up cash flow.

Car’s depreciate fastest in the first 3 years of their lives. After that, your depreciation slows and the annual cost of ownership goes down. (You can read more about car depreciation in my blog on Buying vs. Leasing). You can save money on car insurance by continuing to drive your cheaper car. This is because when you buy a new car, you usually buy a more expensive car that will cost more to replace. So the insurance company charges you more for agreeing to take on the larger risk. Lastly, when you own a car for a longer-term than your car payment, you end up paying off your loan and providing yourself more cash flow. Having no car payment allows you to accelerate retirement savings, debt payment, or overall life enjoyment!

Financing or Cash?

Car financing is cheap right now, and by cheap, I mean interest rates are low. However, you can have great financing and still buy more car than you need. The issue with financing is it tends to shift our focus from the total price we pay for the vehicle to a “manageable”monthly payment. To combat this, I recommend paying cash for a car because it hurts more to spend saved money vs. loaned money. However, financing is a viable option if it means having a more reliable or slower depreciating car that suits your needs and comes at a fair price. One of the best lenders I have found who has reasonable rates and will lend for vehicles over ten years old is PenFed.

What Should I Look For In A Car?

I might channel my inner Click and Clack from CarTalk here:

- Cars typically lose around 60% of their value in the first five years of their life, so if you are trying to stretch your dollar, consider 3 to 5 year-old cars (or older!)

- Purchase a car that depreciates slowly, like a Jeep Wrangler, Toyota Tacoma, or Nissan Frontier.

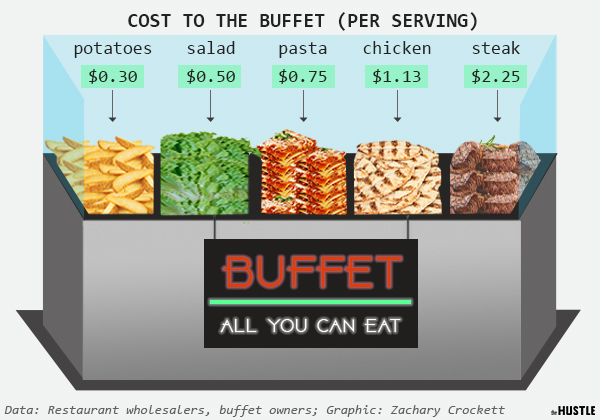

- Purchase a car that is reliable and has low maintenance costs. Lucky for us, yourmechanic.com (a mobile mechanic) has compiled their maintenance data into a chart below that shows the average 10-year maintenance cost by the brand. You can read more about this report HERE.

Why are Used Car Prices High Right Now?

I am always poking around the interweb for used Toyota 4runners. I have no idea why I love them, but I do. And recently, prices seemed to be high, so I did some research, and it turns out that used car prices nationwide are higher than average. But don’t take my word for it; here’s a podcast by planet money discussing how coronavirus has played a role in disturbing the used car market “The Case of The Soaring Car Prices.”

Four Reasons Supply Is Lower

- Manufacturing slowed and stopped in many locations.

- Car repossessions dropped and were even illegal in some states as part of coronavirus relief for consumers. This isn’t all because they care though, financing companies didn’t want a large number of auto loan payments to stop coming in at once.

- A lower number of people rented cars, which reduces their mileage, and delays the rental companies selling their inventory to the used market.

- Increased lease extensions.

Four Reasons Demand Is Up

- Stimulus checks and generous unemployment assistance combined with reduced consumer spending means buyers have more disposable income.

- People are afraid of public transport and buy a car for fear of getting sick

- People work from home now and may not need the high MPG’s and trade their car for an SUV or Truck. (This is more of a change in demand preference)

- Low-interest rates make cars more accessible.

What Works For Me

I’m 27 and have never paid more than $6,500 for a car, and I pile up the highway miles between Greensboro, Charlotte, and Boone. Also, my maintenance expenses are meager (mainly because I DIY, a lot), and insurance costs are even lower. I have included a video that shows a few low-cost car options for someone who may be in the frugal car range of sub $5,000. Of course, low priced cars come with their downsides, for instance, it took me four hours to make a two-hour drive because three spark plugs weren’t firing, Maaco paint jobs are occasionally used, and I actually still have the cassette tape that hooks up to the I-phone to play my music (yes it sounds scratchy). Trust me, I want a heated steering wheel as much as the next guy, but I’d rather spend that $3k option on a mountain bike. The Nukeproof reactor 290 alloy pro if you’re wondering. We all have our weaknesses…

Rule of Thumb

This 10% to 30% rule will not apply to every scenario, however, it is a great place to start the conversation. And after reading the data/thought stream above, I believe you will be a more informed consumer. Both in what your price range should be and in what other variables you should be aware of when it comes to purchasing a vehicle.

Stephen Boatman

Latest posts by Stephen Boatman (see all)

- How to Calculate and Maximize Your Social Security Benefit - May 19, 2023

- An Unaffordable Housing Market: Why and What’s Next? - March 14, 2023

- $500 Billion Student Loan Forgiveness Update ($10k/$20k, New IDR Plan, 0% Interest Ending) - October 20, 2022