Market Commentary Q1 – 2015

When Millie and I got married, we had a wedding shower where people gave us marital wisdom to go along with their gift. I remember hearing cutesy advice like “don’t waste all the good kid names on your pets” and “soak up these first years, they are so much fun.” They were sweet and sincere and made me look forward to being married. But I also remember getting advice from couples who had smile lines on their faces, looked like they still loved each other, but somehow said things like: “marriage is really hard; you have to work at it” and “you have to learn to say you’re sorry…a lot…and mean it.” That wasn’t really what I wanted to hear; and it frankly gave me a pit in my stomach. But what I didn’t realize at the time was that the advice I liked hearing wasn’t actually helpful at all. Who cared if we wasted a good baby name on the dog? And how does one “soak up” years exactly? Rather, it was the honest advice from still happy couples, learned through years of experience that has been the most helpful (however hard as it was to digest.)

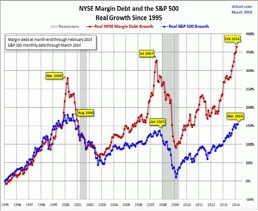

A prospective client found us online and called about a month ago asking to speak to one of our brokers. He was less than amused when I told him “we don’t have any of those, just fiduciary financial planners and advisors.” I didn’t even get a chance to ask any questions before he told me how much money he had and asked me what returns we could get him. I told him the only thing I could guarantee was that our estimate would be wrong, but he wanted it anyway. So finally, I shared that according to our data (see chart above), bonds bought in times like today typically return below 3% and stocks purchased in times like these also tended to perform well below average. I also shared that while these starting points determine very little over the short term (i.e. anything can happen over the next year or two), they were great predictors of what his long term returns would be.

He laughed and said, “Man, that’s too low for me…you’re going to need to do better than that.” I told him we base our expectations on the facts available to us and adjust the risk to our clients’ needs, but yes: for many people it won’t be enough. However, we know it is better to hear the real expectations at the beginning of a marriage (or a financial plan) than afterward. The caller didn’t stay on the phone long before he went on to find someone who would tell him what he wanted to hear.

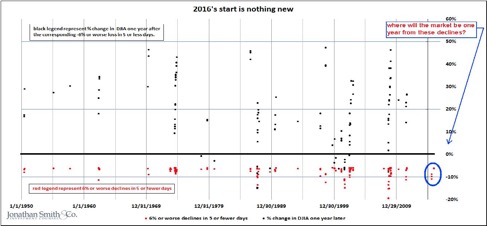

The hottest topic for debate in investing today centers around interest rates: where are they going, when, and what impact will they have on other asset prices? It has been nearly a decade since we’ve experienced an increase in the Federal Funds Rate (which has been flat for the last seven years). The futures market is pricing in expectations for future increases (see in red on previous page) and therefore unless we see a deviation from these rates, there shouldn’t be a large surprise in the equity market either. Even though the sample size is small, it is worth looking at what happened over previous year rate hikes. The top charts show the S&P 500 (in green) increasing along with rates and the bottom charts show 10 year US Treasury yields (in blue) increase and prices fall over the same rate hikes (which are shown in white).

However, investors living through these time periods did not have the convenience to pack up their investments and lock in gains once the chart ended. We know too well that following the time periods illustrated in the second and third columns of charts, came large bear markets brought on by forces far bigger than Fed tightening. And even though we’ve recovered since those bear markets, the reality of living through those time periods while dependent on an investment portfolio or maxing out 401(k) contributions in the face of a declining balance is very hard to stomach.

That is why we think the most important “realistic expectations” that investors need to establish (or revisit) revolve around why they are investing. When I asked that caller why he needed higher returns, he replied, “because I need to have more than I do right now.” This is the same method many of us employ when we’re running late out the door on the way to vacation. The safer options are to either start packing sooner (save more money, earlier in our careers) or change our expectations about when we need to arrive (adjusting our standard of living). Instead, many try to speed along faster than we should (much like taking on more risk than we can stomach or chasing investment returns.) Or worse, we keep the speed the same and simply seesaw between worrying about our arrival time or blindly neglecting that we’ll be late but doing nothing about the problem. The only rational reaction today to being late (whether to retirement, college savings, or vacation) is to embrace the risks we’re capable of stomaching and today’s investment opportunity set, then adjust our expectations accordingly.

Justin Smith

Latest posts by Justin Smith (see all)

- Tariffs and a Declaration of Parental Independence - April 11, 2025

- Quarter in Charts – Q1 2025 - April 11, 2025

- Quarter in Charts – Q4 2024 - January 22, 2025