Market Commentary Q3 – 2015

"It's just like riding a bike...on water."

That’s what I told myself this past July as a boat full of my buddies cheered me on. The five of us had gathered in North Carolina from as far away as Texas and Illinois for our Financial Planning Study Group retreat and I wasn’t going to let them go home without seeing me relive my glory days and attempt a backflip on the wakeboard.

“Attempt” was the operative word. My body did not get along with gravity as well as I remembered and, as you can see in the video still frames, I landed mostly on my face. As I floated there, all my fond memories of wakeboarding were soon crowded out as I remembered what it was like to fall on my face; somehow I had forgotten.

Snapped Back to Reality.

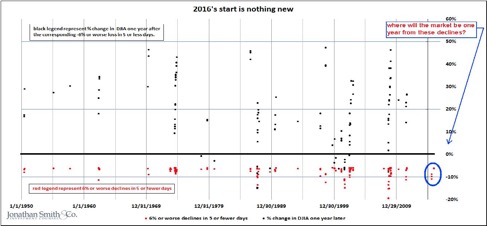

We’ve had 21,863 investing days since October 2, 1928 and so the 218 days with the biggest losses comprise the bottom 1%…what we refer to in inter-office shorthand as simply “Worst Days.” As we have noted in previous commentaries, it had been 4 years since we had experienced a Worst Day. That changed on August 24th as the Dow dropped 1,000 points in the first 10 minutes. The index ended down 3.57% for the day, ranking it as the 192nd Worst Day since 1928 (in the bottom 1%.) Even though we saw a slight rebound over the rest of the week, one thing is certain: investors now remember what a face plant feels like.

It is human nature to try to place a “why” to the fluctuating numbers on a chart. The headlines always read “stocks did X because of Y.” The problem with that that sort of reasoning is that stocks themselves don’t actually DO anything…people (and computer programs to an extent) DO something. The danger with saying “stocks went down because of some series of events” is the implication that the corresponding price decline was rational. The more appropriate (but less headline-friendly) way to describe price declines as a result of human reactions would be something like “buyers were not willing to pay as much because of x” or “it seems sellers really wanted to get out because of x.” This is why Benjamin Graham’s statement rings true: “in the short run, the market is a voting machine but in the long run, it is a weighing machine.”

“I’m confused. Is this the voting machine part or the weighing machine part?” – Tom Brakke, CFA

I read the above quote on Twitter and realized that Tom (a qualified speaker, researcher, and advisor) hit it on the head. Most investors know that the short-term fluctuations are just a voting machine (solely people’s best guesses, feelings, and opinions) but the hard part of investing is that the “long term” is a result of many “short terms.” The cause of the excessive and pessimistic “voting” this quarter seemed to stem from two sources: China and the Fed. Uncertainty over China’s economic future (specifically slowed growth of GDP) combined with restrictive market regulations to cause a 25% decline in Chinese stocks in the third quarter. The ripples only went out from there: the fears of China’s impact on trade and commodities travelled into other foreign markets. Buyers became more hesitant, sellers became more desperate and prices fell.

The other factor that contributed to the price fluctuation was the continued uncertainty over interest rates. Investors have been betting on an increase in interest rates. However, as fears of China’s problems grew, the Fed decided to keep interest rates low and the US markets dipped. On the surface, low interest rates seem like a gift; why would the market drop at the news of continued lowered rates? Just like a mother is concerned when her trouble-prone 10 year-old son shows up with a bouquet of flowers…because she knows there’s likely a broken window somewhere. Likewise, investors worry that the Fed’s bouquet of low interest rates is a sign of a broken economy somewhere.

We do not know what the short run voting machine will crank out for the remaining part of this year or in the years to come. However, we do think the market is within the range of what “normal” investing looks like. Meaning that in the past, when conditions have looked like they do today (prices, earnings, interest rates, GDP growth), investors have been rewarded in the long run for keeping their money invested.

That does not mean we will have straight lines of market appreciation. “Normal” investing means there will be plenty of drawdowns. To the left is a chart from Morgan Housel at The Motley Fool (who gives thanks to Michael Batnick at Ritholtz Wealth Management). It shows the S&P 500 in black and in the background, we see all periods when the index was below its all-time high, represented by different colors. We have been at a market high 7% o f the days an d between 0% and 55% below the high

(white area) 36% of the days. We’ve been where we are today, at 5-10% below the high, for 15% off the days (grey area.). More surprising,, we’ve been 10-20%% below all-time highs for 22% of the days (blue area) and finally 20% or moore below thee high for 21% of the days (red area.) To summarize, we’ve been in territory like today (or lower) for 68% of the last 60 years. In other words, investors could spend most of their days (93%% of them) fondly remembering their previously higher account balances. However avoiding drawdowns is rarely the point of investing.

Housel also shows the 5 year returns for the S&PP 500 following market drawdowns of varying degrees (chart right). Over all periods, there is an 80% chance that the S&&P 500 will bee higher in 5 years and on average, it will be 47%% higher; we think those are great odds. And the only way to improve on those odds? Invest after (and rebalance during) a drawdown. If we believed that anyone could consistently predict and avoid market downturns, that would obviously be preferred (emotionally, i f not financially). But since “face plants” are unavoidable, we think staying in the water and getting back up is the next best thing.

Our comments about the economy and the stock market are based on our own analysis and are not representative of the future performance of any security, fund or of the overall market. Any discussion of specific securities is provided for informational purposes only and should not be deemed as a recommendation to buy or sell.

Justin Smith

Latest posts by Justin Smith (see all)

- Tariffs and a Declaration of Parental Independence - April 11, 2025

- Quarter in Charts – Q1 2025 - April 11, 2025

- Quarter in Charts – Q4 2024 - January 22, 2025