The SECURE Act

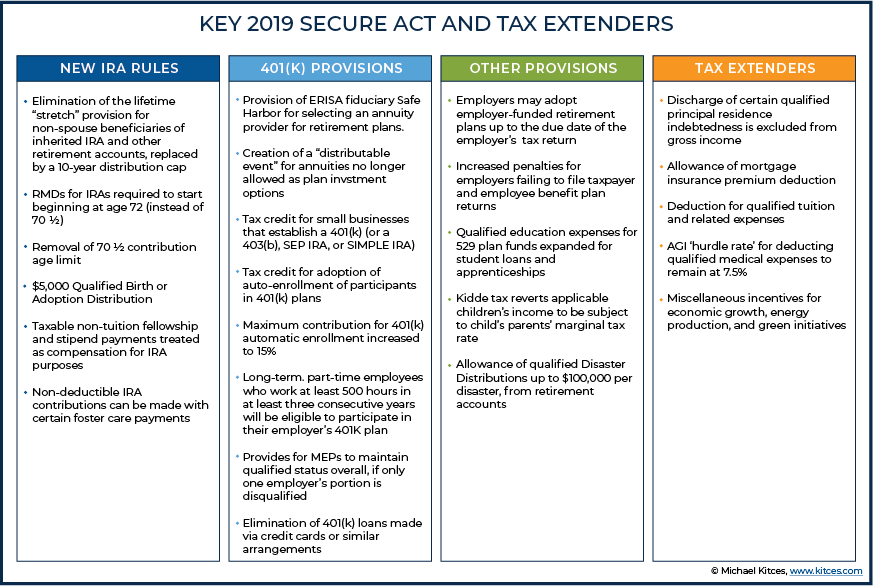

President Trump signed The SECURE Act of 2019 (Setting Every Community Up for Retirement Enhancement of 2019), into law on December 20, 2019. While it has a far-reaching scope (see the chart below from Michael Kitces’ in-depth summary,) in this post, I’ll focus on a few provisions likely to affect most workers, retirees, and 401k and IRA beneficiaries.

The Death of the “Stretch” IRA

With the Act, the law compressed the term over which many beneficiaries pay taxes on inherited IRAs by killing the feature that tacked on years for an inherited IRA to grow tax-deferred before distributions begin. Being able to delay IRAs over the beneficiary’s natural life was known as the stretch IRA. The stretch will still be available to “Eligible Designated Beneficiaries” spouses, minor children (not grandchildren), chronically ill, persons with disabilities, or anyone within ten years of age of the deceased.

An Example

Consider a ninety-year-old IRA holder owning a $250,000 IRA who dies, leaving a fifty-year-old adult child beneficiary. We’ll look at the total required distribution before and after the Act. No one can guarantee the performance of any investment, however, in this illustration, I’m estimating the IRA would grow at 3% per year. I’m also spreading distributions equally over the ten year period.

Before the Act, the beneficiary’s first ten years of RMDs would have been $83,800.30, and with further RMDs occurring over the beneficiary’s lifetime. After the Act, assuming the beneficiary withdraws 1/10 per year, distributions will be $286,596.99, after ten years.

Financial experts claim the Baby Boomer generation will transfer $30 trillion of wealth when they die, the most significant transfer of wealth in history. I expect much of the wealth to wind up in the hands of younger beneficiaries. But, instead of stretching distributions out over the beneficiary’s lifetime, the Act now means the beneficiary will pay the IRS much sooner than before the Act.

For non-spouse inheritors in high-earning, high tax-bracket years during the ten-year window, the IRS will be happy, but beneficiary taxpayers won’t. Careful financial planning could create an otherwise overlooked bonus. By timing the required distribution to coincide with a beneficiary’s potentially low-tax-bracket year, the beneficiary could minimize taxes.

IRA Contributions, Distributions at 72, and Qualified Charitable Distributions (QCD)

After the Act, Individuals who hadn’t become 70 ½ by December 31, 2019, may continue making IRA contributions as long as they have earned income. In addition, the Act doesn’t require distributions until 72. The Act also permits QCDs at age 70 ½, which could lower taxes from a distribution.

Any Other Concerns?

Before the Act, retirement plan trustees’ concerns over high expenses, complicated language, and lock-up provisions, kept annuities in a small percentage of plans (~10%.) Insurance and securities lobbies pushed Congress to get annuities on 401k menus and the lobbies won. The insurance/securities industry is understandably delighted. With the Act, now retirement plan sponsors have a safe harbor exemption from Fiduciary responsibility as long as the annuity carrier attests to having met representations, which in my view are too low, from the insurance carrier.

Better Your Chances

The following sources might be useful: The Wall Street Journal, the 401k Specialist, and Kitces.com. If you’re unable to access the links, we’ll be glad to send you a copy. Finally, before making any investment or estate planning decisions predicated on the SECURE Act, we would welcome you talking with us to confirm that your proposed choices fit all areas of your financial plan.

Jonathan Smith

Latest posts by Jonathan Smith (see all)

- 5 Emotional Roadblocks that Could Halt a Successful Estate Plan - April 16, 2021

- Shining the Light on Hunger in the Darkest of Times - January 1, 2021

- The SECURE Act - January 15, 2020